Understanding what is a health insurance claim? : Explore the intricacies of benefit specifications, provider conditions, and eligibility criteria for health.

Introduction: What is a Health Insurance Claim?

Navigating the complex world of health insurance claims can be overwhelming for policyholders, with its intricate terminology and procedures. This guide is designed to help you navigate the process, whether you’re filing your first claim or seeking to better understand your insurance policy.

We’ll start with the basics of what is a health insurance claim? is, and then delve into the specifics of different plan types, such as HMOs and PPOs. We’ll also provide a step-by-step guide to mastering the filing process, and highlight common pitfalls that can lead to claim denials.

But we won’t stop there. We’ll also offer expert insights into the review process, and provide actionable advice on how to effectively appeal denied claims. This guide is an essential resource for anyone looking to secure their health insurance benefits with confidence. With our guidance, you’ll be able to navigate the complexities of health insurance claims with ease and peace of mind.

Understanding What is a Health Insurance Claim? : A Comprehensive Guide

Definition of Health Insurance Claim

At its core, a health insurance claim is a formal request submitted by a policyholder to their health insurance company. This request is for the payment of the services received from a healthcare provider. Essentially, it’s the bridge between receiving medical services and having your insurance company cover the cost, subject to the terms of your policy.

Understanding the intricacies of a what is a health insurance claim? is foundational for navigating the healthcare system effectively.

When a claim is filed, it undergoes a process of review by the insurance company to ensure that the services rendered are covered under the policyholder’s plan. If approved, the insurer will pay the healthcare provider directly or reimburse the policyholder, depending on the policy’s structure.

- Direct Billing: In many cases, healthcare providers submit claims directly to the insurance company on behalf of the patient, simplifying the process.

- Reimbursement: Policyholders may pay out-of-pocket for services and then submit a claim for reimbursement.

Grasping the definition and workflow of a health insurance claim empowers policyholders to manage their healthcare financing more adeptly.

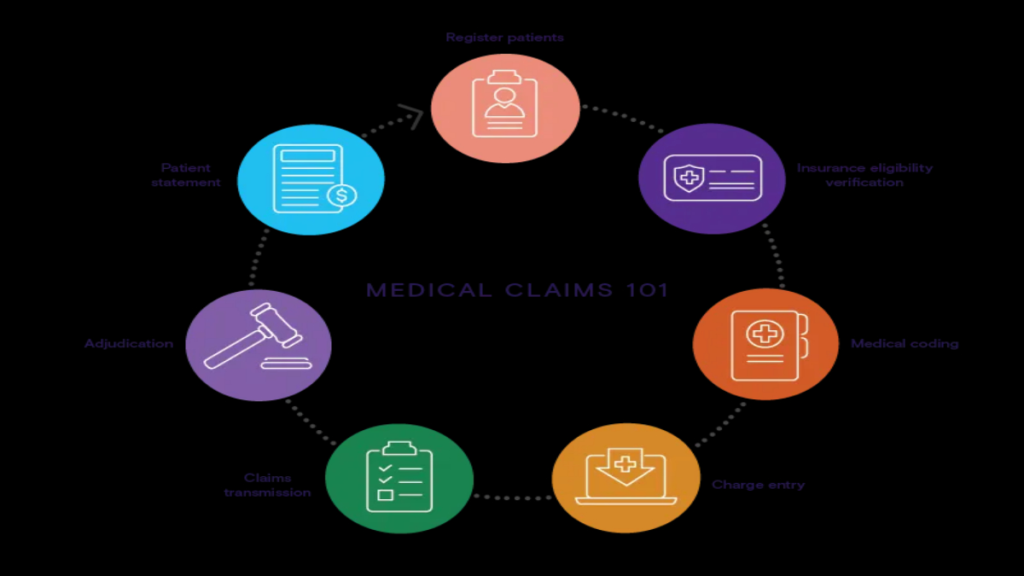

What is a Health Insurance Claim?: Steps to File a Claim

- Gather Necessary Information: This includes detailed invoices from the healthcare provider, the diagnosis, and proof of payment if the claim is for reimbursement.

- Complete the Claim Form: Fill out your insurer’s claim form accurately. Details matter here to avoid delays.

- Submit the Claim: Send the claim form along with all required documentation to your insurance company, adhering to their guidelines for submission.

- Follow Up: Keep in touch with your insurance company to track the status of your claim and provide any additional information if requested.

Filing a health insurance claim might seem daunting, but understanding the step-by-step process can demystify it, ensuring policyholders are reimbursed in a timely manner.

Timely filing is crucial; delays can lead to denied claims. Keeping a record of all communications and submissions can help safeguard against such issues.

Types of Health Insurance Claims

- Pre-Authorized Claims: These are claims for services that require pre-approval from the insurance company before the service is rendered. This is common for expensive or specialized treatments.

- Direct Billing Claims: Here, the healthcare provider submits the claim directly to the insurance company, eliminating the need for the patient to pay upfront.

- Reimbursement Claims: In this scenario, the policyholder pays out-of-pocket at the time of service and later submits a claim to be reimbursed by the insurance company.

Each type of claim serves a different purpose and understanding which one applies to your situation can streamline the process of seeking medical services and ensuring they are covered.

Choosing the right type of claim to file can significantly affect the ease of processing and the time it takes to receive benefits.

Navigating through the different types of health insurance claims enhances a policyholder’s confidence in managing their healthcare finances effectively.

Common Reasons for Claim Denial

Understanding why claims are denied can help policyholders avoid common pitfalls. Some frequent reasons include:

- Service Not Covered: The policy does not cover the healthcare service received.

- Information Errors: Incorrect or incomplete information on the claim form.

- Lack of Pre-Authorization: Failure to obtain required pre-authorization for certain services.

- Exceeding Benefit Limits: The claim exceeds the policy’s coverage limits.

Arming yourself with knowledge of these common issues can preempt mistakes, ensuring a smoother claim process.

Engaging with your insurance company to clarify coverage details and claim procedures before receiving services can mitigate the risk of denial. This proactive approach not only ensures that you are fully aware of your benefits but also places you in a stronger position to contest any denials that may occur.

Taking steps to understand the reasons behind claim denials can lead to more successful claim submissions and less financial strain from out-of-pocket healthcare costs.

Filing Your Health Insurance Claim: A Step-by-Step Process

Preparing Your Claim Documentation

Embarking on the journey of what is a health insurance claim?

begins with the meticulous process of gathering essential documents. This foundational step is critical as it sets the stage for a smooth claim submission. Policyholders should start by collecting all medical bills, receipts, and any correspondence from healthcare providers related to the treatment. These documents serve as the backbone of your claim, providing tangible proof of the services received and the expenses incurred.

- Detailed medical bills: Ensure that each bill includes the date of service, the type of service provided, and the charge for each service.

- Prescription receipts: If medications are part of your claim, gather all related receipts, highlighting the name of the medication, the prescribing doctor, and the cost.

- Proof of payment: Any receipts showing payments made towards your treatment are vital to establish the out-of-pocket expenses you’re seeking reimbursement for.

Moreover, understanding your health insurance policy is paramount. Familiarize yourself with the covered benefits, policy limits, deductibles, and co-payment requirements. This knowledge will guide you in preparing your documentation accurately and in aligning your expectations regarding the claim outcome.

Remember, the goal is not only to submit a claim but to do so with the confidence that you have provided all necessary information for a favorable review.

After organizing your documents, the next step is to complete the claim form provided by your insurance company. Pay close attention to detail, fill out each section thoroughly, and double-check for accuracy. A well-prepared dossier of documents and a correctly filled claim form are your best allies in the claim process. Now, with everything in order, you’re ready to move to the next phase: submitting your claim to the insurance company.

Submitting Your Claim to the Insurance Company

Once your claim documentation is prepared, the next step is submitting it to your insurance company. This phase can often be navigated through online portals provided by insurers, though some may require mailing physical documents. When submitting online, ensure that all digital copies of your documents are clear and legible. If mailing your claim, consider using certified mail to track the delivery of your documents.

- Online submission: Check your insurance company’s website for instructions on how to submit your claim online. This method is often faster and allows for easier tracking of your claim’s status.

- Mail submission: If required to mail your documents, keep copies of everything you send. The tracking number from certified mail will be crucial for confirming the insurer’s receipt of your claim.

After submitting your claim, the waiting game begins. It’s prudent to note the date of submission and set reminders to follow up. Most insurance companies will provide an acknowledgment of receipt, either through email or mail. This acknowledgment is a good sign that your claim is under review.

A successful submission is marked by thorough documentation and adherence to the submission guidelines of your insurance company. It demonstrates your proactive approach and attention to detail.

The anticipation of the review process can be daunting, but knowing that you have submitted a well-documented and timely claim can provide a sense of relief. The next stage is understanding what happens behind the scenes as your claim is being reviewed.

Understanding the Insurance Company’s Review Process

The review process is where your insurance company evaluates your claim to determine coverage eligibility. This critical phase involves a detailed assessment of your submitted documents against your policy’s coverage. Insurance adjusters will scrutinize medical bills, treatment records, and your policy to ensure that the claim is valid and falls within the scope of your coverage.

- Verification of Coverage: The first step is confirming that the policy was active during the time of treatment and that the services rendered are covered benefits.

- Assessment of Documentation: Each document you submitted is reviewed for accuracy and completeness. Missing or unclear information may lead to delays or denial.

- Determination of Liability: The adjuster will ascertain if any other insurance could be liable for some or all of the costs.

During this time, it’s not uncommon for the insurance company to request additional information or clarification. Responding promptly to these requests is vital to keep the process moving forward.

Patience and cooperation are key during the review process. Engaging with your insurance company in a constructive manner can help resolve any issues swiftly.

Once the review is complete, you will receive a decision. If approved, you will be informed of the payment amount and when to expect it. However, not all claims are approved on the first try. Understanding the steps to take if your claim is denied is crucial for a possible reversal of the decision.

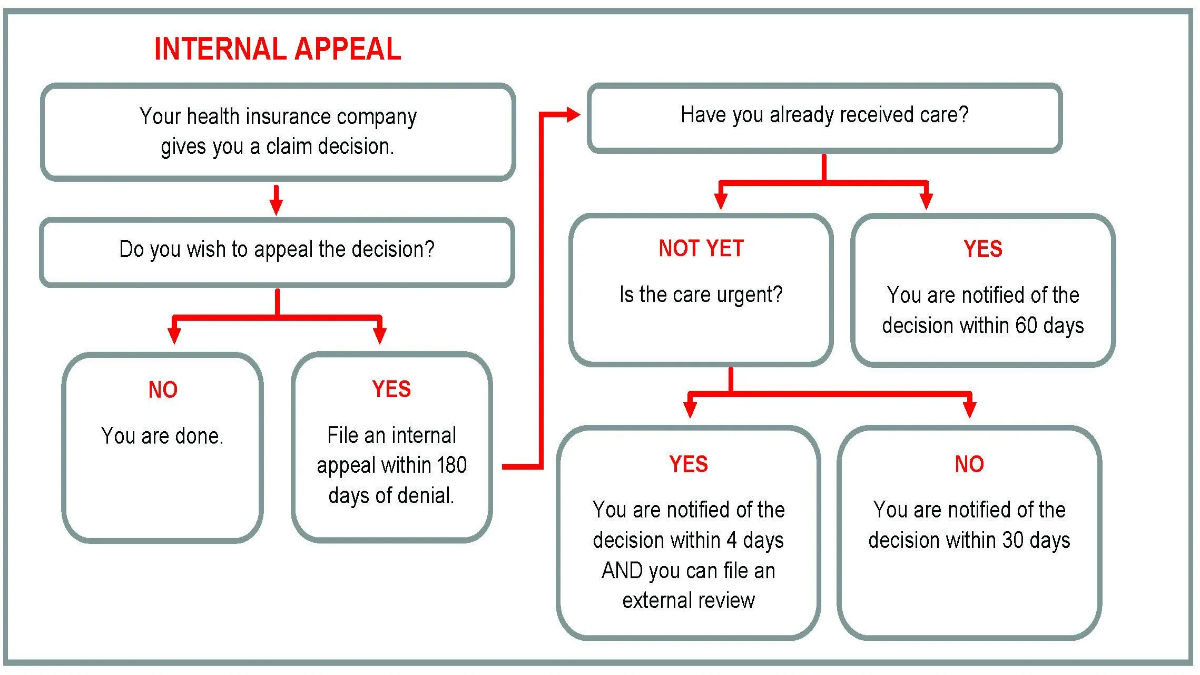

What to Do If Your Claim Is Denied

Receiving a denial on your health insurance claim can be disheartening, but it’s not the end of the road. The denial notice should clearly state the reason for rejection. Common reasons include incomplete documentation, services not covered under your policy, or the insurance company’s inability to verify the necessity of the treatment.

- Review the denial letter carefully: Understand the specific reasons for the denial and the appeal process outlined by your insurance company.

- Gather additional information: If the denial is due to incomplete information, compiling the missing documents or obtaining further details from your healthcare provider may be necessary.

- Write an appeal letter: Clearly state why you believe the claim should be covered and include any additional evidence to support your case.

An appeal is your opportunity to present your case from a different angle or provide new information that could influence the decision. It’s crucial to adhere to the appeal process timelines and requirements as specified by your insurance company.

Remember, persistence is key. Many denied claims are overturned on appeal, especially when additional supporting documentation is provided.

The journey of filing a health insurance claim, from preparing your documentation to appealing denials, requires patience, attention to detail, and perseverance. Each step taken with diligence increases the likelihood of a favorable outcome. Embark on this process armed with knowledge, and let each step you take be a stride towards securing the benefits you’re entitled to.

Decoding the Types of Health Insurance Claims: From HMOs to PPOs

HMO vs. PPO: Understanding Your Plan

When exploring health insurance options, two common types you will encounter are Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). Each has distinct features that can significantly influence your healthcare experience and the nature of your insurance claims.

HMO plans typically require you to choose a primary care physician (PCP) who becomes your main point of contact for all health-related issues. This structure emphasizes preventive care and requires referrals for specialist consultations, impacting how claims are processed and approved.

On the other hand, PPO plans offer more flexibility by allowing direct access to specialists without needing a referral. This can lead to a broader range of claims but may involve higher out-of-pocket costs. Understanding the nuances between these plans is crucial for making informed decisions about your healthcare.

- Referral Requirements: HMOs often necessitate referrals for specialist services, potentially delaying care but managing costs effectively.

- Out-of-Network Coverage: PPOs provide out-of-network coverage, albeit at higher costs, offering more choice in healthcare providers.

Choosing between an HMO and a PPO affects not only your access to healthcare services but also the way your insurance claims are handled. A thorough comparison of these plans will help you navigate your healthcare journey more confidently and ensure that your insurance plan aligns with your medical needs and lifestyle preferences.

In-Network vs. Out-of-Network Claims

The distinction between in-network and out-of-network providers is pivotal in understanding health insurance claims. In-network providers have agreements with your insurance company to provide services at negotiated rates, directly influencing the cost and processing of claims.

Choosing an in-network provider usually means lower out-of-pocket expenses and less paperwork for you, as these providers directly bill the insurance company. Out-of-network claims often involve higher costs and require you to pay upfront and submit claims for reimbursement.

- Cost Differences: In-network claims are generally more cost-effective than out-of-network claims, due to pre-negotiated rates.

- Reimbursement Process: Submitting out-of-network claims involves more steps, including paying upfront and managing reimbursement paperwork.

Understanding the impact of your provider network choice on the cost and hassle of claims can drastically improve your healthcare experience. This knowledge empowers you to make informed decisions that align with your financial and healthcare needs.

Emergency vs. Non-Emergency Claims

Emergency and non-emergency health insurance claims are treated differently by insurance providers, with each type having specific procedures and implications for policyholders. Emergency claims often require immediate attention, bypassing the usual pre-authorization processes and sometimes even the network status of the healthcare provider.

In the context of an emergency, insurers are required to cover necessary services, irrespective of the provider’s network status, although the definition of ’emergency’ can vary between plans.

- Pre-Authorization: Non-emergency claims may require pre-authorization, ensuring that the proposed medical services are covered under your policy.

- Network Considerations: While emergency services are typically covered regardless of the network, non-emergency services might be covered differently based on the provider’s network affiliation.

Understanding these distinctions helps you navigate the claims process more effectively, ensuring that you receive the care you need while also managing costs efficiently. Being informed about your plan’s procedures for both emergency and non-emergency claims can significantly impact your healthcare journey.

Pre-Authorized vs. Post-Service Claims

In the realm of health insurance claims, pre-authorization and post-service claims represent critical phases. Pre-authorized claims involve obtaining approval from your insurance company before receiving certain healthcare services, which helps ensure that the services are covered under your policy and are medically necessary.

This preemptive step is often required for expensive or specialized services and serves as a way to manage healthcare costs effectively while ensuring patient care aligns with insurance policy standards.

- Pre-Authorization Process: Involves submitting a request for approval before undergoing specific healthcare services, reducing the risk of claim denial.

- Post-Service Claim Submission: Entails submitting a claim after receiving healthcare services, which may or may not have been pre-authorized.

Navigating pre-authorized and post-service claims efficiently can lead to a smoother healthcare experience, minimizing the risk of unexpected expenses and claim rejections. Familiarizing yourself with your plan’s requirements for pre-authorization can ensure that you are well-prepared for both planned and unforeseen healthcare needs.

Navigating Health Insurance Claim Denials: Steps to Take for Resolution

Understanding Why Claims Are Denied

Before diving into the appeal process, it’s crucial to understand why health insurance claims are denied. Common reasons include errors in the claim form, services not covered under your policy, or lack of pre-authorization. Identifying the specific reason is the first step towards resolving the issue.

Understanding the denial reason is pivotal; it shapes your appeal strategy.

- Lack of Pre-Authorization: Many insurance plans require pre-authorization for certain services. Failing to obtain this can lead to claim denial.

- Non-Covered Services: Every policy has exclusions. Services not covered by your policy will be denied.

- Misinformation or Errors: Simple mistakes on claim forms can result in denials, stressing the importance of accuracy.

After pinpointing the denial reason, prepare to gather evidence and documentation to support your appeal. This initial understanding can significantly increase the chances of overturning the denial.

How to Appeal a Denied Claim

Once you know why your claim was denied, the next step is launching an appeal. Start by reviewing your insurance policy to understand the appeals process. This often involves writing an appeal letter, including evidence such as medical records or a letter from your healthcare provider.

- Review Insurance Policy: Familiarize yourself with the appeals process detailed in your policy.

- Write an Appeal Letter: Clearly state why you believe the denial was incorrect, attaching supporting documents.

- Gather Documentation: Medical records, doctor’s letters, and any other relevant information should be compiled to support your case.

- Submit Within Deadlines: Be aware of and adhere to any deadlines for filing an appeal to avoid forfeiting your right to challenge the denial.

Patience and persistence are key during this process. It may take time, but effectively presenting your case increases the likelihood of a favorable outcome.

The Role of Documentation in Appeal Success

Documentation is the backbone of a successful appeal. It speaks when words cannot.

Securing the right documentation is critical. This includes detailed medical records, letters of necessity from your healthcare provider, and any correspondences with your insurance company. Each piece of evidence should directly support your reason for appealing the denial.

- Medical Records: These provide a detailed account of your treatment and are essential for substantiating your claim.

- Letter of Necessity: A letter from your healthcare provider explaining the medical necessity of the denied service.

- Insurance Correspondences: Any prior communications with your insurance company regarding the claim or service in question.

Organizing your documentation systematically can make your appeal more compelling and easier for the insurance company to review. This meticulous approach can lead to a successful overturn of the denial.

Legal Avenues for Disputed Claims

If your appeal is unsuccessful, exploring legal avenues may be the next step. This can include seeking assistance from a legal professional who specializes in insurance law or contacting your state’s insurance commissioner’s office. These resources can offer guidance and, in some cases, directly intervene on your behalf.

- Consult an Insurance Lawyer: A legal professional can provide advice on your rights and the feasibility of further legal action.

- Contact State Insurance Commissioner: This office can offer assistance and, in some cases, mediate disputes between policyholders and insurance companies.

- Consider Small Claims Court: For smaller claims, small claims court can be a quicker and less expensive option.

While taking legal action can seem daunting, it’s sometimes necessary to ensure you receive the benefits you’re entitled to. Armed with the right information and support, policyholders can navigate these challenges and achieve a resolution.

Conclusion: What is a Health Insurance Claim?

Navigating the world of what is a health insurance claim? requires knowledge and determination. Understanding HMOs, PPOs, in-network vs. out-of-network claims, and mastering filing and appeals empower you to advocate for your health confidently. This guide emphasizes thorough documentation and proactive communication with your insurer. Use these insights to manage claims effectively, safeguarding your well-being. Stay informed, take control, and stride towards a healthier future.

FAQs: What is a Health Insurance Claim?

What is a Health Insurance Claim?

A health insurance claim is a request made by an insured individual to their health insurance company for the payment of medical services received. It is the process by which policyholders inform their insurer about the healthcare services they have received, so the insurer can either reimburse the policyholder or pay the healthcare provider directly.

How do I file a health insurance claim?

To file a health insurance claim, you typically need to collect and prepare all relevant documentation, including medical bills and proof of treatment. Then, submit these documents along with a completed claim form to your insurance company. Be sure to follow your insurer’s guidelines for submission, which may vary depending on your plan and the type of claim.

What are the main types of health insurance claims?

There are two main types of health insurance claims: reimbursed claims and direct billing claims. In reimbursed claims, the policyholder pays for the healthcare services out-of-pocket and then submits a claim to get reimbursed by the insurance company. In direct billing claims, the healthcare provider sends the bill directly to the insurance company, which then pays the provider without requiring upfront payment from the policyholder.

Why was my health insurance claim denied?

Claims can be denied for several reasons, including services not covered under your policy, missing or incorrect information in the submitted documentation, or failure to pre-authorize services when required. Understanding the specific reasons for the denial, as provided by your insurance company, is crucial for addressing the issue.

How can I appeal a denied health insurance claim?

If your claim is denied, you have the right to appeal the decision. Start by reviewing the denial letter from your insurance company to understand the reason for denial. Then, gather all relevant documentation, such as medical records and letters from your healthcare provider, and submit an appeal form or letter to your insurance company, outlining why you believe the claim should be covered. Following your insurer’s appeal process is crucial for a successful appeal.

What is the difference between HMO and PPO insurance plans when filing claims?

HMO (Health Maintenance Organization) and PPO (Preferred Provider Organization) plans differ mainly in the flexibility they offer for choosing healthcare providers and in how claims are processed. With an HMO, you typically need to choose a primary care physician within the network, and referrals are required for specialist services. Most services are covered only if you use in-network providers, and claims are often directly billed. PPOs offer more flexibility, allowing you to see specialists without referrals and use out-of-network providers, though at a higher cost. PPO claims may require you to pay upfront and seek reimbursement, especially for out-of-network services.