Does windscreen claim count as a claim? : Learn about the definition, importance, and implications of windscreen claims in the context of auto insurance.

Introduction: Does windscreen claim count as a claim?

Driving with a damaged windscreen is not just unsafe—it can also be a complex affair when it comes to insurance claims. Understanding windscreen claims and how they impact your insurance is crucial for every driver. With the right knowledge, you can navigate the process smoothly, from filing a claim to protecting your no-claims bonus. Whether you’re dealing with a tiny chip or a full crack, knowing the difference between comprehensive and third-party coverage, and how your insurer treats windscreen claims, can save you time and money.

This article offers a comprehensive guide on everything you need to know about does windscreen claim count as a claim?. We’ll walk you through the step-by-step process of filing a claim, the documentation you’ll need, and how to interact with your insurance provider efficiently. Additionally, we provide insights into selecting the best insurance policy for windscreen coverage, ensuring you’re fully protected on the road. Dive into the nuances of windscreen claims and make informed decisions that keep your insurance premiums in check.

Understanding Windscreen Claims: Do They Affect Your Insurance?

Defining Windscreen Claims

When we talk about windscreen claims, we’re referring to the process of notifying your insurance company about damage to your vehicle’s windscreen that requires repair or replacement. This might seem straightforward, but the implications and procedures can vary significantly. Understanding the nuances of these claims is crucial for any vehicle owner.

A windscreen claim is not just about fixing glass; it’s a declaration to your insurer that your vehicle has sustained damage that could affect its structural integrity and safety on the road.

- Initiation: The process begins when the policyholder contacts their insurer to report the damage. This step is critical and should be done as soon as possible to avoid further complications.

- Assessment: An assessment follows, often requiring a professional evaluation to determine if the windscreen can be repaired or needs replacement.

- Resolution: Based on the assessment, the insurer will authorize a repair or replacement, typically through a network of approved service providers.

The ability to navigate a windscreen claim effectively hinges on understanding these steps and the policyholder’s responsibilities. Ensuring you have comprehensive coverage can mitigate many of the potential headaches associated with these claims.

Impact on Insurance Premiums

Many vehicle owners worry about the impact of a Does windscreen claim count as a claim? on their insurance premiums. It’s a valid concern, as insurers assess risk and adjust premiums based on a policyholder’s claim history. However, the effect of a windscreen claim can vary.

- Minor Impact: In many cases, especially with comprehensive policies, a single windscreen claim may not significantly affect your premiums. Insurers often view these as non-fault claims, especially if caused by unavoidable road hazards.

- Frequency Matters: Multiple claims within a short period can signal to insurers that you pose a higher risk, potentially leading to increased premiums.

- Policy Terms: Some insurers offer windscreen cover as an optional extra, with specific terms regarding claims and premium adjustments. Understanding these can help manage potential cost implications.

Being proactive about windscreen damage and choosing the right insurance policy can help minimize the impact on your premiums. Reviewing your policy’s fine print and discussing coverage options with your insurer can provide clarity and help you make informed decisions.

Differences Between Comprehensive and Third-Party Coverage

Understanding the distinction between comprehensive and third-party insurance coverage is pivotal for grasping how windscreen claims are handled.

- Comprehensive Coverage: Offers the broadest protection, including for windscreen damage. Policies typically cover the cost of repair or replacement, minus any applicable deductible.

- Third-Party Coverage: Provides the most basic level of insurance, covering damage to others caused by you. It does not usually include windscreen damage, leaving you to shoulder the cost.

Choosing comprehensive over third-party coverage can significantly affect your peace of mind and financial protection in the event of windscreen damage. It ensures that you’re covered for a wide range of incidents, beyond just liability for damage to others.

Vehicle owners should weigh the benefits of comprehensive coverage against the potential increase in premiums. It often proves to be a prudent investment, safeguarding against unexpected expenses and contributing to the vehicle’s longevity and safety.

How Insurers Treat Windscreen Claims

Insurers have varying approaches to handling windscreen claims, influenced by policy details, the nature of the damage, and the claimant’s history. It’s important to understand these nuances to navigate claims smoothly.

- Claim Process: Typically involves reporting the damage, undergoing assessment, and then repair or replacement. Insurers aim to streamline this process, often offering a list of approved service providers.

- Deductibles: Many policies require the payment of a deductible for windscreen claims. This amount can vary, and in some cases, insurers offer plans with no deductible for windscreen damage.

- Impact on No-Claims Bonus: A key concern for many, some insurers do not penalize policyholders for windscreen claims, recognizing the frequent inevitability of such damage.

Understanding your insurer’s specific procedures and policies regarding windscreen claims can save time and avoid unnecessary stress. Regularly reviewing your policy and maintaining open communication with your insurer can help ensure that you’re adequately covered and fully aware of your entitlements and obligations.

Maintaining a clear and proactive stance on vehicle insurance, especially concerning windscreen damage, can contribute significantly to your vehicle’s upkeep and ensure you’re well-protected against unforeseen incidents. Engaging with your insurance provider to clarify the specifics of your coverage can lead to better informed and more confident vehicle ownership.

Does Windscreen Claim Count as a Claim?: A Step-by-Step Guide

Initiating a Claim: First Steps

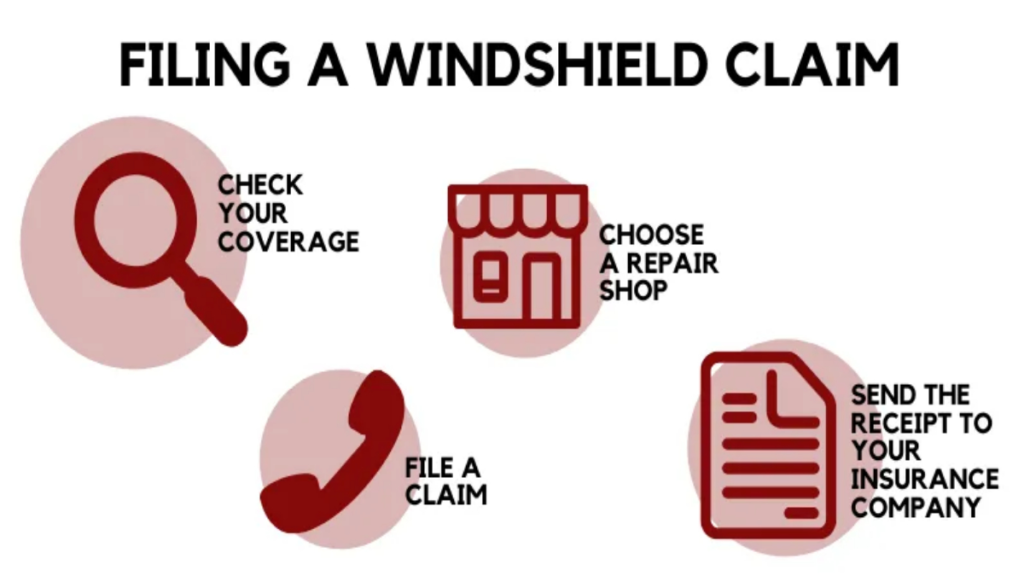

Embarking on the journey of does windscreen claim count as a claim? starts with understanding the initial steps that are essential for a smooth process. The moment you notice damage to your windscreen, it’s crucial to assess the extent. Not all damages require a full claim; sometimes, a repair is sufficient and more cost-effective.

- Assess the Damage: Determine whether the windscreen can be repaired or needs replacement. This decision is pivotal in the claim process.

- Contact Your Insurance Provider: Reach out to your insurer to report the damage as soon as possible. This step initiates the claim process.

- Review Your Policy: Familiarize yourself with your policy details, specifically coverage related to windscreen damage, to understand what costs you may be liable for.

- Gather Essential Information: Prepare all necessary personal and vehicle details that your insurer will require to process the claim.

Remember, the key to a successful claim starts with swift action and clear communication with your insurance provider. By following these steps, you set a strong foundation for the rest of the claim process.

Documentation Needed for a Windscreen Claim

- Proof of Insurance: Your insurer will require proof of your current insurance policy. This document verifies your coverage and is the first step in validating your claim.

- Photographic Evidence: Photos of the windscreen damage from multiple angles can provide clear evidence of the extent and nature of the damage.

- Incident Report: If the damage was the result of an accident, a detailed report of the incident can be crucial for the claim.

- Repair or Replacement Quotes: Obtaining quotes from approved service providers will give your insurer an estimate of the claim’s cost.

Gathering the necessary documentation is a critical step in the claim process. It not only helps in substantiating your claim but also in expediting the approval process. Make sure to keep copies of all documents submitted for your records.

Interacting With Your Insurance Provider

Once you have initiated your claim and gathered the necessary documentation, the next step involves direct interaction with your insurance provider. This stage is crucial for clarifying any doubts and understanding the next steps. Ensure to ask about the estimated timeline for claim processing, any deductible costs, and if they require additional information.

Effective communication with your insurance provider can significantly impact the efficiency of the claim process. Don’t hesitate to ask questions or seek clarification on any aspects of your claim.

During these interactions, keep detailed records of all communications, including the names of the representatives you speak with, dates, and the information discussed. This record can be invaluable if there are any discrepancies or issues later on.

Remember, your insurance provider is there to assist you through this process. Keeping the lines of communication open and clear will facilitate a smoother claim experience.

Timeline for Claim Processing and Approval

Understanding the timeline for claim processing and approval is essential for setting realistic expectations. Typically, the time frame can vary depending on the complexity of the claim, the insurer’s policies, and the responsiveness of both parties. Most insurers aim to process claims within a few days to a few weeks.

- Immediate Response: Insurers usually acknowledge receipt of a claim within a few days of submission.

- Assessment Period: The insurer will assess the claim, which may involve an inspection of the windscreen damage.

- Decision Time: Following the assessment, the insurer will make a decision on the claim and inform you of the outcome.

- Settlement: If the claim is approved, the insurer will proceed with the settlement, which includes repair or replacement of the windscreen.

The timeline can be influenced by how promptly and accurately you submit all required documentation and respond to any inquiries from your insurer. Patience and cooperation are key to a favorable outcome, and keeping informed of the process can help manage expectations.

Will My No-Claims Bonus Be Affected by a Windscreen Claim?

Understanding the No-Claims Bonus

The no-claims bonus (NCB) is a reward mechanism that insurance companies offer to policyholders who do not make any claims during their policy period. Essentially, it’s a way to acknowledge and incentivize safe driving and careful ownership. The longer you go without filing a claim, the higher the bonus or discount you may receive on your insurance premium in subsequent years.

“The no-claims bonus is a testament to a driver’s ability to avoid accidents and claims, serving as a barometer for risk and careful driving.”

It’s crucial to understand that the NCB is accumulative, increasing with each claim-free year. However, certain types of claims can have an impact on your no-claims bonus, leading to concerns among policyholders about whether filing for specific claims, like those for windscreen damage, could affect their accrued bonuses.

- Accumulative Nature: The bonus builds up over years, offering potentially significant discounts.

- Impact of Claims: Not all claims are treated equally; some may affect your NCB, while others might not.

Knowing how different claims affect your NCB is essential for maintaining your discount level and making informed decisions about when to file a claim.

Conditions Under Which Windscreen Claims Affect the Bonus

Windscreen claims occupy a unique position in the landscape of car insurance claims. Given that windscreen damage can arise from many uncontrollable factors like road debris, it’s common to wonder if such a claim could impact your prized no-claims bonus.

“While some insurers may not penalize you for a windscreen claim, others might have specific policies in place.”

Several conditions determine the effect of a windscreen claim on your NCB:

- Policy Terms: Your insurer’s policy terms are the primary determinant. Some policies explicitly exclude windscreen claims from affecting the NCB, while others do not.

- Type of Claim: A repair claim is often viewed differently from a replacement claim, with the former less likely to impact your NCB.

- Excess Payment: Whether or not you pay an excess can also influence the outcome.

It’s advisable to review your insurance policy documents or speak directly with your insurer to understand the specific conditions under which a windscreen claim might affect your no-claims bonus. This proactive approach ensures you’re well-informed before any need to file a claim arises.

Insurance Policies and Windscreen Claims

Insurance policies vary significantly in how does windscreen claim count as a claim?, especially concerning the no-claims bonus. While some insurers offer windscreen cover as a standard part of comprehensive policies, others may offer it as an optional extra. This difference in policy structure is crucial in determining whether a windscreen claim will affect your NCB.

“Understanding your policy’s stance on windscreen claims is pivotal in safeguarding your no-claims bonus.”

- Comprehensive Coverage: Policies with inclusive windscreen cover typically allow for at least one no-fault claim without affecting the NCB.

- Optional Windscreen Cover: Opting into additional windscreen cover may provide more lenient terms regarding your NCB.

Given these variations, it’s beneficial to familiarize yourself with your policy’s specifics. If your current coverage doesn’t align with your needs or concerns regarding the NCB, it might be time to discuss alternatives or adjustments with your insurer.

Protecting Your No-Claims Bonus

For many drivers, the no-claims bonus is a valuable asset in reducing insurance costs. Protecting this bonus, therefore, becomes a priority, especially when faced with the need to make a claim. Fortunately, there are strategies to safeguard your NCB even when filing windscreen claims.

Firstly, consider NCB protection cover, an optional addition that allows you to make a certain number of claims without affecting your bonus. While this cover can increase your premium, it offers peace of mind and financial benefits in the long run.

- Review Your Policy: Understand the specifics of your policy regarding windscreen claims and the NCB.

- NCB Protection Cover: Investing in NCB protection can be a wise decision if you’re concerned about potential claims.

- Consider the Claim’s Necessity: Sometimes, it might be more economical to pay for minor repairs out of pocket rather than risking your NCB.

Exploring these avenues not only helps in maintaining your no-claims bonus but also ensures that you make the most out of your insurance policy. Engaging in a dialogue with your insurer can further personalize your coverage, aligning it with your priorities and concerns about your NCB.

Choosing the Right Insurance Policy for Windscreen Coverage

Key Features of an Ideal Windscreen Cover

When delving into the realm of vehicle insurance, pinpointing the perfect windscreen coverage can seem daunting. Yet, understanding the key features is essential. An optimal policy not only covers the cost of glass repair and replacement but also ensures that no claim bonus (NCB) remains unaffected. This feature is paramount as it preserves your insurance benefits even after a windscreen claim.

“A comprehensive windscreen cover should seamlessly integrate with your overall vehicle insurance, offering peace of mind against unforeseen damages.”

- Zero Deductible Options: Some policies offer the advantage of no deductible for windscreen repairs, meaning you won’t have to pay out of pocket for minor damages.

- Unlimited Claims: Look for a policy that allows for multiple claims without penalizing your premium rates, ensuring continuous coverage.

- Wide Network of Authorized Repair Shops: Accessibility to a broad network of approved service centers can significantly ease the repair process.

Choosing a policy with these features will not only safeguard your vehicle’s aesthetics but will also contribute to maintaining its integrity and value.

Comparing Windscreen Coverage Across Different Insurers

Embarking on a comparison journey across different insurers is a critical step towards securing the best windscreen cover. Each provider offers a unique blend of benefits, premiums, and exclusions. Therefore, diligent comparison is necessary to discern the most favorable deal.

- Review Coverage Limits: Assess the maximum amount insurers are willing to cover for windscreen repairs or replacements.

- Examine Premium Adjustments: Understand how windscreen claims might affect your future premiums with each insurer.

- Check for Value-Added Services: Some policies might offer complimentary services like roadside assistance, enhancing the overall value of the cover.

“An informed decision emerges from a thorough comparison, weighing the pros and cons of each insurer’s offering.”

By meticulously analyzing these factors, you position yourself to select a policy that not only meets your immediate needs but also provides long-term satisfaction and security.

Understanding Policy Exclusions

Grasping the intricacies of does windscreen claim count as a claim? cover does not include is as crucial as knowing what it covers. Most policies have exclusions that can affect your claim eligibility. Common exclusions include damages due to wear and tear, lack of maintenance, or if the damage occurred under circumstances violating the policy terms, like illegal activities.

- Wear and Tear: Damages that occur gradually over time are typically not covered.

- Lack of Maintenance: Failing to maintain your windshield in good condition can lead to denied claims.

- Illegal Activities: Any damage incurred during illegal acts is usually excluded from coverage.

Being aware of these exclusions helps in setting realistic expectations and fosters a more transparent relationship with your insurer. It encourages policyholders to maintain their vehicles diligently, ensuring longevity and durability.

Tips for Selecting the Best Windscreen Claim Policy

Selecting the ultimate windscreen claim policy necessitates a blend of foresight and insight. Begin with identifying your specific needs based on your vehicle type, usage, and geographical location. High-risk areas for road debris might require more comprehensive coverage. Moreover, does windscreen claim count as a claim? in detail is essential; it should be straightforward and user-friendly, minimizing stress during what can already be a taxing time.

- Understand the Claims Process: Opt for an insurer with a simple, hassle-free claims process.

- Consider Policy Flexibility: A policy that offers flexibility in terms of repair locations and claim limits is ideal.

- Evaluate Customer Service: Excellent customer support can significantly enhance your experience, especially during claims.

Armed with these insights, you’re better equipped to navigate the complex landscape of windscreen insurance, ensuring your vehicle remains in pristine condition, safeguarded against the unpredictable.

Conclusion

Navigating the intricacies of does windscreen claim count as a claim? and their impact on your insurance doesn’t have to be a daunting task. From understanding the nuances between comprehensive and third-party coverage to mastering the step-by-step guide for filing a claim, this knowledge empowers you to make informed decisions. Remember, the right insurance policy not only protects your no-claims bonus but also offers peace of mind through ideal windscreen cover options. Comparing windscreen coverage across different insurers and knowing what your policy includes and excludes can save you from unforeseen expenses and complications.

As you move forward, consider the importance of protecting your no-claims bonus and the conditions under which a windscreen claim might affect it. Selecting the best windscreen claim policy requires a balance of comprehensive coverage and reasonable premiums. Let this discussion serve as a stepping stone towards securing an insurance policy that meets your needs, encouraging you to delve deeper into the specifics of insurance policies and windscreen claims. Your journey to a more secure automotive future begins now.

FAQs:

Does making a windscreen claim affect my insurance premiums?

Typically, a windscreen claim, particularly under comprehensive insurance policies, does not directly impact your insurance premiums. However, the specifics can vary between insurers, and frequent claims over a short period might influence future premium calculations.

Will a windscreen claim affect my no-claims bonus?

In most cases, filing a windscreen claim will not affect your no-claims bonus. Insurance companies usually treat windscreen repairs or replacements as separate from claims that would impact your no-claims bonus. However, it’s essential to review your policy’s terms or consult with your insurer for confirmation.

What is the process for filing a windscreen claim?

The process involves notifying your insurer about the damage, providing the necessary documentation (which may include photos of the damage, your insurance policy number, and personal identification), and then following your insurer’s guidance for repair or replacement. The timeline and specific steps can vary, so it’s advisable to contact your insurance provider directly for detailed instructions.

What documentation do I need for a windscreen claim?

You’ll generally need to provide proof of insurance, photographic evidence of the windscreen damage, and possibly a police report if the damage was due to vandalism or a road incident. Also, personal identification and any relevant receipts or invoices if you’ve already undertaken any emergency repairs may be required.

How do insurers treat windscreen claims under third-party coverage?

Windscreen damage is typically not covered under third-party only insurance policies. This type of coverage is designed to pay for damage or injuries to others that you’re liable for in an accident, not damage to your own vehicle. For windscreen coverage, you would need comprehensive or a specific windscreen cover.

What should I look for in an ideal windscreen cover policy?

Look for a policy that offers unlimited windscreen repairs and at least one full replacement per year without affecting your no-claims bonus. Additionally, ensure that the policy allows you to use an approved repairer of your choice and does not significantly increase your premium for windscreen claims. Reading the fine print for any exclusions or limitations is also crucial.

insurance | Vacation Home Insurance: Vacation homes require specialized insurance, especially if rented out. MAFA Insurance helps owners find comprehensive coverage that addresses their unique needs.

I’m really glad to hear that my article helped you feel hopeful!