Frustrated by why are my insurance rates going up? You’re not alone. Understand the factors behind the increases and what you can do about it.

Introduction: Why Are My Insurance Rates Going Up?

In recent years, many Americans have noticed a significant increase in their insurance premiums, whether it be health, auto, or home insurance. This trend has prompted questions and concerns about the underlying causes of these rate hikes and what can be expected in the future. In this detailed blog post, we will explore the various factors contributing to the rising insurance costs, offer insights on how to mitigate the impact on your finances, and provide practical advice for choosing the right insurance policies.

Why Are Insurance Rates Going Up?

Economic Factors Influencing Insurance Premiums

The economy plays a crucial role in determining insurance rates. Factors such as inflation, interest rates, and the overall economic climate directly affect how insurance companies price their policies. For instance, higher medical costs due to inflation can lead to increased health insurance premiums.

Impact of Natural Disasters on Insurance Costs

In recent years, the frequency and severity of natural disasters have escalated, significantly impacting the insurance industry. Events like hurricanes, wildfires, and floods require insurers to pay out large claims, which in turn leads to higher premiums for policyholders.

Technological Advancements and Their Double-Edged Sword

While technology has made processing claims and assessing risks easier, it also increases the cost of repairs and replacements. Modern cars and homes equipped with sophisticated technology can be more expensive to fix, leading to higher claims and consequently, higher premiums.

How to Manage Rising Insurance Costs

Shopping Around for Better Rates

One of the most effective ways to manage rising insurance costs is to shop around. Comparing different policies and insurers can help you find the most cost-effective solution without compromising on coverage.

Increasing Deductibles to Lower Premiums

Opting for a higher deductible can significantly lower your insurance premiums. However, this means you will have to pay more out-of-pocket when a claim is made, so it’s important to balance the risk and reward.

Taking Advantage of Discounts and Bundling Policies

Many insurance companies offer discounts for various reasons, such as having multiple policies with the same provider, maintaining a good credit score, or installing safety features in your home or vehicle.

Increased Claims and Severity

- Distracted driving: Texting, talking, or using apps behind the wheel sadly contributes to a greater number of accidents.

- More expensive repairs: Cars packed with technology are fantastic, but those sensors and cameras are costly to repair or replace after a fender bender.

- Medical cost inflation: Healthcare costs in general are rising, and this impacts the cost of treating accident injuries.

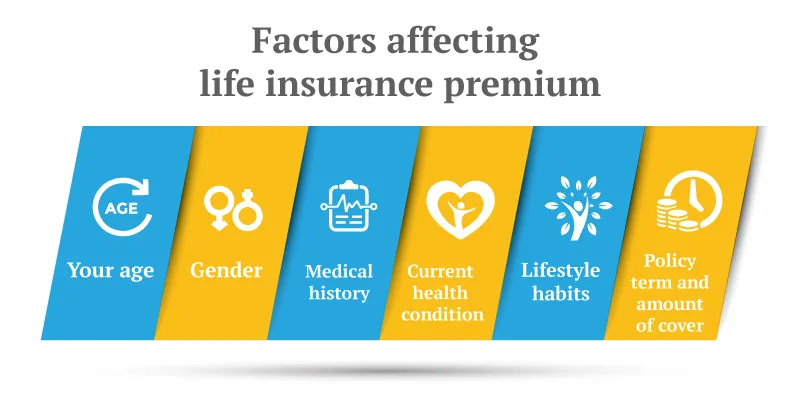

What factors contribute to rising insurance rates?

Rising insurance rates are influenced by a multitude of factors that span economic conditions, environmental changes, technological advancements, and shifts in societal behavior. Understanding these factors can help consumers and businesses alike navigate the complexities of the insurance market. Here are some of the key contributors to increasing insurance premiums:

Economic Inflation

Inflation affects virtually every aspect of the economy, including the insurance industry. As the cost of goods and services increases, the cost for insurers to pay out claims also rises. This is particularly evident in sectors like healthcare and auto insurance, where the cost of medical services and vehicle repairs have steadily increased, leading insurers to adjust premiums accordingly to cover these higher expenses.

Natural Disasters and Climate Change

The increasing frequency and severity of natural disasters, attributed in part to climate change, have a significant impact on insurance rates. Hurricanes, wildfires, floods, and other catastrophic events lead to massive claims, which in turn forces insurance companies to raise premiums to cover these losses. Regions that are particularly prone to such events might experience higher than average rate increases.

Technological Advancements

While technology has improved efficiency and accuracy in risk assessment and claims processing, it also has a downside. The cost to repair or replace technology-laden vehicles and smart homes is considerably higher than their less sophisticated counterparts. As a result, claims costs have risen, contributing to higher premiums. Additionally, cyber insurance rates are climbing as cyber threats become more sophisticated and prevalent.

Health Care Costs

For health insurance, one of the primary drivers of increased premiums is the rising cost of healthcare. This includes the cost of medical procedures, prescription drugs, and hospital care. As these expenses grow, health insurers adjust premiums upward to keep pace with the rising costs of claims.

Regulatory Changes

Insurance is a heavily regulated industry, and changes in legislation can have a direct impact on insurance rates. New laws and regulations regarding coverage requirements, consumer protections, or financial reserves for insurers can lead to increased operational costs for insurance companies, which may be passed on to consumers in the form of higher premiums.

Demographic Shifts

Changes in the demographic landscape, such as an aging population or shifts in driving behavior among younger generations, can also influence insurance rates. For example, an aging population may lead to higher health insurance costs due to increased demand for medical services. Similarly, if data shows a trend in increased accidents among younger drivers, auto insurers may raise premiums for this demographic.

Market Competition and Insurance Fraud

The level of competition among insurance providers in a particular market can influence premium rates. In highly competitive markets, insurers may be pressured to keep rates low to attract customers. Conversely, insurance fraud—ranging from exaggerated claims to outright false claims—increases costs for insurers, which can lead to higher premiums for everyone.Understanding these factors is crucial for consumers looking to make informed decisions about their insurance coverage. By recognizing the reasons behind rate increases, individuals and businesses can better assess their options and potentially find ways to mitigate the impact of rising premiums, such as shopping around for better rates, increasing deductibles, or taking advantage of discounts.

Conclusion:

The rise in insurance rates is influenced by a complex mix of economic factors, natural disasters, and technological advancements. By understanding these factors, consumers can better navigate the landscape of insurance and find ways to manage their expenses. Remember, the key to dealing with rising insurance costs is to stay informed, shop around, and take proactive steps to reduce your risk profile.

Calculator:

To use the insurance rate estimator provided in the HTML document, follow these simple steps:

- Open the Calculator: Open the HTML file in a web browser. You should see a form titled “Insurance Rate Estimator” with dropdown menus for selecting your location, type of insurance, and claims history.

- Select Your Location: Click on the dropdown menu labeled “Your Location” and choose an option that best describes your area. Options might include “High Risk Area,” “Moderate Risk Area,” or “Low Risk Area.”

- Choose Type of Insurance: Next, select the type of insurance you’re interested in from the “Type of Insurance” dropdown menu. Options could include “Auto,” “Home,” or “Health” insurance.

- Indicate Your Claims History: In the “Claims History” dropdown, select an option that reflects your history of insurance claims. Choices might range from “High” to “Moderate” to “Low.”

- Calculate Your Rate: After making your selections, click the “Calculate Rate” button. The calculator will use the inputs you’ve provided to estimate a rate increase, which will be displayed under the button in the “result” section.

- View Your Estimated Rate Increase: The estimated rate increase will appear in green text below the form. This number is a simple calculation based on the factors you selected and serves as an estimate of how much your insurance rate might increase.

Remember, this calculator provides a basic estimation and should be used as a guideline rather than an exact prediction. For precise insurance quotes, it’s best to contact insurance providers directly.

Hi, I’m Jack. Your website has become my go-to destination for expert advice and knowledge. Keep up the fantastic work!

I’m really glad to hear that my article helped you feel hopeful!