Restaurant insurance made easy. Get customized coverage to shield your business risks.

Introduction: Restaurant Insurance

When running a restaurant, protecting your business is crucial. Restaurant insurance provides coverage for various risks that can impact your establishment. Understanding the importance of having the right insurance policy in place can help safeguard your restaurant’s success. In this blog post, we will explore the key aspects of restaurant insurance and why it is essential for your business.

Why Do You Need Restaurant Insurance?

Restaurant insurance is a safety net for your business, protecting it from unexpected incidents that can lead to financial losses. Without proper coverage, a single event can lead to a significant financial burden or even bankruptcy.

Essential Types of Restaurant Insurance

- General Liability Insurance: This policy covers third-party claims of bodily injury, property damage, and advertising injury.

- Property Insurance: Protects your restaurant’s physical assets, including buildings, equipment, and inventory.

- Workers’ Compensation Insurance: Covers medical expenses and lost wages for employees injured on the job.

- Liquor Liability Insurance: If your restaurant serves alcohol, this policy covers legal fees and damages resulting from alcohol-related incidents.

- Business Interruption Insurance: Provides income replacement if your restaurant is forced to close due to a covered event.

How Much Does Restaurant Insurance Cost?

The cost of restaurant insurance varies depending on factors such as location, size, and coverage options. On average, restaurants pay between $1,500 and $3,000 annually for general liability insurance. Property insurance costs depend on the value of your assets, while workers’ compensation insurance rates are based on your payroll.

Top Restaurant Insurance Providers in the US

- The Hartford: Offers a range of insurance policies tailored to the restaurant industry.

- CNA: Provides comprehensive coverage options for restaurants of all sizes.

- Travelers: Offers specialized insurance solutions for restaurants, including cyber liability coverage.

- Liberty Mutual: Provides customizable insurance policies for restaurants, including liability and property coverage.

- State Farm: Offers a variety of insurance options for small and mid-sized restaurants.

What is restaurant insurance and why is it important?

Restaurant insurance is a crucial aspect of protecting your business against various risks and liabilities. It covers potential financial losses due to claims arising from foodborne illnesses, accidents, property damage, and other unforeseen events. By having the right insurance coverage, restaurant owners can safeguard their investments, employees, and customers, ensuring a secure and successful business environment.

There are several types of insurance policies that restaurant owners should consider, including general liability, property, workers’ compensation, and liquor liability insurance. General liability insurance covers third-party claims of bodily injury, property damage, and advertising injury, while property insurance protects your restaurant’s physical assets, such as buildings, equipment, and inventory. Workers’ compensation insurance covers medical expenses and lost wages for employees injured on the job, and liquor liability insurance covers legal fees and damages resulting from alcohol-related incidents.

The cost of restaurant insurance varies depending on factors such as location, size, and coverage options. However, investing in the right insurance policies can provide peace of mind and financial protection, ensuring the long-term success of your business.

When selecting an insurance provider, it’s essential to consider their reputation, coverage options, and customer service. Some top restaurant insurance providers in the US include The Hartford, CNA, Travelers, Liberty Mutual, and State Farm. These providers offer specialized insurance solutions for restaurants, including liability and property coverage, as well as cyber liability coverage.

In summary, restaurant insurance is a vital aspect of protecting your business against various risks and liabilities. By understanding the essential types of restaurant insurance, costs, and top providers in the US, you can make informed decisions and safeguard your business effectively.

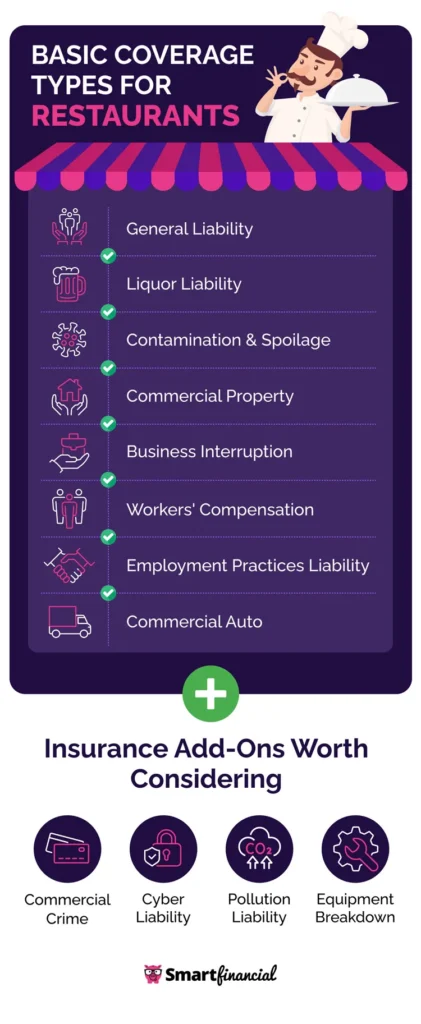

What are the common types of restaurant insurance policies?

Restaurant insurance is a crucial aspect of protecting your business from various risks and liabilities. It covers potential financial losses due to claims arising from foodborne illnesses, accidents, property damage, and other unforeseen events. The most common types of restaurant insurance policies include:

- General Liability Insurance: This policy covers third-party claims of bodily injury, property damage, and personal injury. It is essential for protecting your business from slip-and-fall accidents, property damage, and other common risks.

- Workers’ Compensation Insurance: This policy covers medical expenses and lost wages for employees injured on the job. It is mandatory in most states for businesses with employees.

- Commercial Property Insurance: This policy protects your restaurant’s physical assets, including buildings, equipment, and inventory. It covers damage from events such as fire, theft, and vandalism.

- Business Owner’s Policy (BOP): A BOP bundles commercial property insurance and general liability insurance under one plan, providing comprehensive coverage at a lower cost.

- Food Contamination and Spoilage Insurance: This policy covers the cost of replacing food due to contamination or spoilage, protecting your business from financial losses due to foodborne illnesses or power outages.

- Liquor Liability Insurance: If your restaurant serves alcohol, this policy covers legal fees, property damage, and medical costs if alcohol is served or sold to a visibly intoxicated person who then proceeds to harm others.

- Cyber Liability Insurance: This policy helps restaurants recover from cyberattacks and data breaches, protecting your business from financial losses due to cyber threats.

- Employment Practices Liability Insurance (EPLI): This policy covers your legal costs if an employee decides to sue you for discrimination, harassment, or other employment-related issues.

- Commercial Vehicle Insurance: If your restaurant has vehicles for catering or delivery, this policy covers legal fees, property damage, and medical costs in the event of an accident.

- Hired and Non-Owned Auto Liability Insurance: This policy covers legal fees, property damage, and medical costs if an employee uses their personal vehicle for business purposes and gets into an accident.

These insurance policies are essential for protecting your restaurant business from various risks and liabilities. By understanding the different types of restaurant insurance policies available, you can make informed decisions and safeguard your business effectively.

How to choose the right restaurant insurance policy for your business?

To choose the right restaurant insurance policy for your business, follow these key steps based on the information from the provided sources:

- Assess Your Risks: Before selecting a restaurant insurance policy, assess the specific risks your restaurant faces, such as property damage, liability claims, foodborne illnesses, liquor liability, and business interruption. Understanding your risks is crucial in determining the coverage you need.

- Work with an Experienced Agent or Broker: Navigating the complexities of insurance policies can be daunting, especially for restaurant owners. Seek the expertise of an experienced insurance agent or broker who specializes in restaurant coverage. They can assess your risks, recommend appropriate coverage options, and help you understand the terms and conditions of different policies.

- Understand Types of Coverage: Familiarize yourself with the different types of restaurant insurance coverage available, including general liability, property, workers’ compensation, liquor liability, and business interruption insurance. Knowing the types of coverage will help you tailor your policy to suit your unique needs.

- Compare Multiple Quotes: Don’t settle for the first insurance quote you receive. Shop around and compare quotes from multiple insurers to ensure you’re getting the best coverage at a competitive price. Balance the cost against the benefits of each policy to find the most suitable option for your restaurant.

- Consider Additional Coverages: Depending on your restaurant’s specific needs, consider additional coverages or endorsements to supplement your primary insurance policy. For example, if you offer delivery services, you might need non-owned auto insurance, or if you host events off-site, you may require special event insurance. Tailor your coverage to address all potential risks your business may face.

- Review Policy Limits and Deductibles: Pay close attention to the policy limits and deductibles outlined in each insurance quote. Ensure that the limits are sufficient to cover your potential liabilities and consider how deductibles will impact your finances in the event of a claim. Understanding these details will help you make an informed decision.

- Read the Fine Print: Before finalizing any insurance policy, carefully read the fine print. Pay attention to exclusions, limitations, and any special conditions that may apply. Understanding what is and isn’t covered by your policy is essential to avoid surprises in the future.

- Reassess Regularly: As your restaurant evolves and grows, your insurance needs may change. Regularly reassess your coverage and make adjustments as necessary. Changes such as expanding your menu, adding new locations, or increasing your staff may require updates to your insurance policy to ensure you’re adequately protected.

By following these steps and considering the advice from the sources provided, you can make an informed decision when choosing the right restaurant insurance policy for your business.

What are the risks that restaurant insurance can protect against?

Restaurant insurance can protect against various risks that restaurant businesses may face, including:

- Property Damage: This includes damage to the restaurant’s physical property, such as the building, equipment, and inventory, due to events like fire, water damage, theft, and vandalism.

- Liability Claims: Restaurants can be held liable for incidents such as slip and fall accidents or foodborne illnesses. Liability insurance can help cover the costs of legal claims made against the restaurant by customers or employees.

- Employee Injuries: Restaurants can purchase workers’ compensation insurance to cover the costs of medical bills and lost wages for employees injured on the job.

- Business Interruption: This refers to any event that disrupts the restaurant’s operations, resulting in a loss of income. Business interruption insurance can help cover the costs of lost revenue and expenses incurred due to the disruption.

- Cyber Attacks: Restaurants can purchase cyber liability insurance to help cover the costs of a cyber attack, such as theft of customer data or financial losses.

These insurance policies can help protect the restaurant’s financial stability and reputation, providing peace of mind and enabling the business to focus on providing great food and service to its customers.

How to find the best restaurant insurance policy for your business?

To find the best restaurant insurance policy for your business, follow these steps:

- Assess Your Risks: Identify the specific risks your restaurant faces, such as property damage, liability claims, foodborne illnesses, liquor liability, and business interruption.

- Understand Types of Coverage: Familiarize yourself with the different types of restaurant insurance coverage available, including general liability, property, workers’ compensation, liquor liability, and business interruption insurance.

- Work with an Experienced Agent or Broker: Navigate the complexities of insurance policies with the help of an experienced insurance agent or broker who specializes in restaurant coverage. They can assess your risks, recommend appropriate coverage options, and help you understand the terms and conditions of different policies.

- Compare Multiple Quotes: Shop around and compare quotes from multiple insurers to ensure you’re getting the best coverage at a competitive price. The cheapest option may not always offer the most comprehensive coverage, so weigh the cost against the benefits of each policy.

- Consider Additional Coverages: Depending on your restaurant’s unique needs, consider additional coverages or endorsements to supplement your primary insurance policy. For example, if you offer delivery services, you might need non-owned auto insurance to cover liability risks associated with employees using their vehicles for work.

- Review Policy Limits and Deductibles: Pay close attention to the policy limits and deductibles outlined in each insurance quote. Make sure the limits are sufficient to cover your potential liabilities, and consider how the deductibles will impact your finances in the event of a claim.

- Read the Fine Print: Before finalizing any insurance policy, take the time to read the fine print carefully. Understand what is and isn’t covered by your policy to avoid surprises down the road.

- Reassess Regularly: As your restaurant evolves and grows, your insurance needs may change. Regularly reassess your coverage and make adjustments as necessary to ensure you’re adequately protected.

By following these steps, you can find a restaurant insurance policy that suits your unique needs and provides comprehensive coverage for your business.

What is the cost of restaurant insurance policies worldwide?

The cost of restaurant insurance policies can vary significantly worldwide, depending on factors such as the size and location of the restaurant, the type of cuisine served, and the specific insurance coverage required. However, some general guidelines can be derived from the search results provided.

In the United States, a low-cost package of restaurant liability insurance with business personal property and rental premises coverages can cost around $299 per year. However, the cost can range significantly based on the specific needs and risk profile of the restaurant. For instance, general liability insurance for restaurants can range from $529 to $6,097 annually, with an average annual payment of around $950. A Business Owner Policy (BOP) for restaurants can range from $1,100 to $10,500 annually, with an average annual payment of around $2,160. Workers’ compensation insurance for restaurants can range from $600 to $10,000 annually, with an average annual payment of around $1,500. Liquor liability insurance for restaurants can range from $350 to $3,000 annually, with an average annual payment of around $620.

These costs can vary based on the specific coverage needs of the restaurant, the location, and the insurer. It is essential to shop around and compare quotes from multiple insurers to ensure that you are getting the best coverage at a competitive price. Additionally, taking steps to reduce risk, such as offering safety training to workers, can help keep premiums low.

It is important to note that these costs are specific to the United States and may not be representative of the cost of restaurant insurance policies worldwide. Factors such as local laws and regulations, cultural differences, and economic conditions can significantly impact the cost of restaurant insurance in other countries. Therefore, it is essential to research and compare costs specific to your location and needs.

What is the process for filing a claim with a restaurant insurance policy?

The process for filing a claim with a restaurant insurance policy typically involves the following steps:

- Contact Your Insurance Provider: Notify your insurance provider as soon as possible after the incident occurs. Most insurance companies have specific procedures for filing claims, and they can guide you through the process.

- Gather Documentation: Collect all relevant documentation related to the incident, including photos, videos, witness statements, police reports (if applicable), and any other evidence that supports your claim.

- Complete Claim Forms: Your insurance provider will likely require you to fill out claim forms detailing the nature of the incident, the damages incurred, and any other relevant information. Ensure that you provide accurate and detailed information to expedite the claims process.

- Submit the Claim: Once you have gathered all the necessary documentation and completed the claim forms, submit them to your insurance provider. Be sure to follow their specific instructions for claim submission.

- Cooperate with Inspections: Your insurance provider may conduct inspections to assess the damages and verify the information provided in your claim. Cooperate with these inspections and provide access to the relevant areas of your restaurant.

- Negotiate Settlement: After reviewing your claim, the insurance company will determine the coverage and compensation you are entitled to. If there are any discrepancies or issues with the settlement offer, you can negotiate with the insurance adjuster to reach a fair resolution.

- Receive Settlement: Once the claim is processed and approved, you will receive a settlement from your insurance provider to cover the damages and losses incurred as per the terms of your policy.

By following these steps and working closely with your insurance provider, you can effectively file a claim with your restaurant insurance policy and receive the necessary support to recover from unexpected incidents or damages.

What factors should be considered when choosing a restaurant insurance policy?

When choosing a restaurant insurance policy, several factors should be considered to ensure that you select the most suitable coverage for your business. These factors include:

- Assessing Your Risks: Understand the specific risks your restaurant faces, such as property damage, liability claims, foodborne illnesses, liquor liability, and business interruption. Identifying these risks will help tailor your insurance coverage to address potential vulnerabilities effectively.

- Working with an Experienced Agent or Broker: Collaborate with an experienced insurance agent or broker who specializes in restaurant coverage. They can assess your risks, recommend appropriate policies, and negotiate competitive rates on your behalf. Providing accurate and up-to-date information about your business is crucial for them to recommend the most suitable coverage options.

- Understanding Types of Coverage: Familiarize yourself with the different types of restaurant insurance coverage available, such as general liability, property, workers’ compensation, liquor liability, and business interruption insurance. Knowing the types of coverage will help you make informed decisions about the best policy for your establishment.

- Comparing Quotes and Policies: After identifying your restaurant’s insurance needs and consulting with an insurance professional, compare quotes and policies from multiple insurers. Look beyond the premium cost and consider factors like the scope of coverage, exclusions, the insurer’s financial stability, and customer service quality. This comparison will help you find the best coverage at a competitive price.

- Considering Additional Coverages: Depending on your restaurant’s unique needs, consider additional coverages or endorsements to supplement your primary insurance policy. For example, if you offer delivery services, you might need non-owned auto insurance, or if you host events off-site, you may require special event insurance. Tailoring your coverage to address all potential risks is essential.

- Reviewing Policy Limits and Deductibles: Pay close attention to the policy limits and deductibles outlined in each insurance quote. Ensure that the limits are sufficient to cover your potential liabilities and consider how deductibles will impact your finances in the event of a claim. Understanding these details will help you make an informed decision.

- Reading the Fine Print: Before finalizing any insurance policy, carefully read the fine print. Pay attention to exclusions, limitations, and any special conditions that may apply. Understanding what is and isn’t covered by your policy is crucial to avoid surprises in the future.

By considering these factors when choosing a restaurant insurance policy, you can ensure that your business is adequately protected against potential risks and liabilities.

How to compare quotes from different insurance providers for restaurant insurance policies?

To compare quotes from different insurance providers for restaurant insurance policies, follow these key steps based on the information from the provided sources:

- Start with Reputable Insurance Carriers: Request quotes from dependable insurance carriers with strong financial ratings. Ensure that the insurance companies you consider are reputable and financially stable to guarantee they can fulfill claims when needed.

- Consider More Than Just Insurance Rates: Avoid making decisions solely based on the cost of premiums. Focus on finding the best protection for your business rather than opting for the cheapest option. Look beyond the price and assess the coverage, policy limits, and exclusions to ensure you are getting comprehensive protection.

- Understand What’s Covered – and What’s Not: Review each policy carefully to understand the coverage options and exclusions. Compare the details of what is covered under each policy to ensure it aligns with your business’s specific needs and potential risks.

- Pick a Policy That Can Grow with Your Business: Consider how your business might grow in the future when comparing insurance quotes. Choose a policy that can accommodate your business’s expansion and evolving needs to avoid the hassle of changing policies as your business grows.

- Review Policy Limits and Deductibles: Pay attention to the policy limits and deductibles outlined in each insurance quote. Ensure that the limits are sufficient to cover your potential liabilities and consider how deductibles will impact your finances in the event of a claim. Understanding these details will help you make an informed decision.

- Read the Fine Print: Before finalizing any insurance policy, carefully read the fine print to understand exclusions, limitations, and any special conditions that may apply. Being aware of what is and isn’t covered by each policy will help you avoid surprises in the future.

By following these steps, you can effectively compare quotes from different insurance providers for restaurant insurance policies and select the most suitable coverage for your business.

What are the consequences of not having restaurant insurance for your business?

Not having restaurant insurance for your business can lead to significant financial consequences and risks. Restaurants face unique risks, including liability claims, food contamination, employee-related concerns, and property damage. Without insurance, a liability claim can result in substantial medical costs, legal fees, and potential settlements, which could lead to financial ruin. Food contamination can lead to illness among patrons, resulting in medical expenses and potential legal action. Employee-related concerns, such as harassment or wrongful termination claims, can also result in costly legal fees and settlements. Property damage, whether from natural disasters or accidents, can lead to expensive repair or replacement costs.

Moreover, without insurance, you may not be able to meet legal requirements, such as workers’ compensation insurance for employees, which could result in fines or legal action. Additionally, not having insurance could make it difficult to secure loans or partnerships, as many lenders and businesses require proof of insurance before working with a restaurant.

In summary, not having restaurant insurance can expose your business to significant financial risks and legal liabilities, making it crucial to have adequate insurance coverage to protect your business and its assets.

Conclusion: Restaurant Insurance

Protecting your restaurant business with the right restaurant insurance coverage is crucial for long-term success. By understanding the essential types of restaurant insurance, costs, and top providers in the US, you can make informed decisions and safeguard your business from unexpected events.

FAQs: Restaurant Insurance

Q: What is the minimum restaurant insurance coverage required by law?

A: Workers’ compensation insurance is mandatory in most states for businesses with employees. General liability insurance may also be required in certain states or cities.

Q: Can I bundle my restaurant insurance policies?

A: Yes, many insurance providers offer bundling options, which can save you money and simplify your coverage.

Q: What is the difference between general liability and property insurance?

A: General liability insurance covers third-party claims of bodily injury, property damage, and advertising injury. Property insurance covers your restaurant’s physical assets, including buildings, equipment, and inventory.