Standard fire insurance can save your home from costly repairs. Discover affordable coverage options today. Secure your property now!

Introduction: Standard Fire Insurance

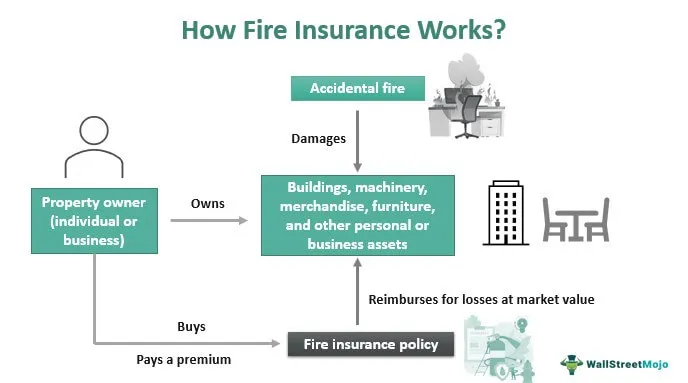

Standard fire insurance is a crucial protection that provides coverage for damages caused by fires to your property. Understanding the basics of this insurance can help you safeguard your assets and have peace of mind. Let’s delve into the key aspects of standard fire insurance to help you make informed decisions.

Fire devastates in moments, but the right standard fire insurance policy becomes your financial firewall, safeguarding your future. Navigating the intricate world of standard fire insurance policies can overwhelm the best of us. From understanding what your policy covers to mastering the claims process, and maximizing your coverage, this article is your comprehensive guide. We delve into the essentials of choosing the right standard fire insurance policy, the step-by-step claims process post-disaster, strategic tips to enhance your insurance protection, and how to compare providers to find your perfect match. Whether you’re assessing your current policy or on the hunt for new coverage, our insights will empower you to make informed decisions, ensuring you’re well-protected against the unforeseen.

Amidst the complexities of standard fire insurance, clarity emerges through knowing the key exclusions, mastering claim filings, and understanding how to bolster your coverage. With the right knowledge, you can navigate the aftermath of a fire with confidence and secure your financial recovery. This article is your roadmap to optimizing standard fire insurance coverage, designed to illuminate the path from policy selection to claim settlement, ensuring peace of mind in the face of adversity.

Understanding Standard Fire Insurance Policies

What Standard Fire Insurance Covers

Standard fire insurance policies are pivotal for homeowners, renters, and business owners seeking to safeguard their property from the devastating impacts of fire. These policies primarily offer financial compensation for damages or losses to buildings, personal property, and other assets resulting from fire. Understanding the scope of coverage is essential to maximizing the benefits of your policy.

It’s not just about repairing the physical damage; it’s about restoring your peace of mind.

- Building Coverage: This aspect of the policy pertains to the structural integrity of your home or business premises. It includes compensation for repairs or rebuilding efforts necessitated by fire damage.

- Personal Property: Whether you’re a homeowner or a renter, your belongings are covered under this section. It ranges from furniture and appliances to personal items, provided they’re damaged by fire.

- Additional Living Expenses (ALE): If a fire renders your home uninhabitable, ALE helps cover the costs associated with temporary housing and other living expenses during the repair period.

Understanding the breadth of coverage can significantly assist in selecting a policy that aligns with your needs. Remember, the exact coverages can vary by provider, so thorough comparison is key.

Key Exclusions to Know

While standard fire insurance offers comprehensive protection against fire damage, certain exclusions are universally applied. Recognizing these exclusions is critical in managing your expectations and identifying potential gaps in your coverage.

- Intentional Acts: Any damage arising from fires set intentionally by the policyholder or with their consent is not covered.

- War and Nuclear Hazard: Losses resulting from war-related activities or nuclear hazards are typically excluded from coverage.

- Wear and Tear: Standard policies do not cover damages attributed to normal wear and tear or deterioration over time.

Additionally, specific natural disasters that lead to fire, such as earthquakes and floods, may require separate coverage. It’s advisable to consult with your insurance provider to understand these exclusions fully and consider additional policies if necessary.

Knowledge of these exclusions empowers you to make informed decisions about supplementary coverage.

How to Choose the Right Policy for You

Selecting the appropriate standard fire insurance policy demands a clear understanding of your needs and a comprehensive evaluation of available options. Factors such as the value of your property, location, and personal risk tolerance play a crucial role in this decision-making process.

Choosing the right policy is not just about the cost; it’s about ensuring adequate protection for your most valuable assets.

- Assess Your Needs: Begin by evaluating the total value of your property and possessions. This assessment will guide you in determining the amount of coverage necessary to protect your assets fully.

- Compare Policies: Investigate the coverage options, exclusions, and premiums offered by different insurance providers. Look for policies that offer the best balance of comprehensive coverage and affordability.

- Consider Additional Coverages: Depending on your location and specific risk factors, consider purchasing additional coverages such as flood or earthquake insurance to complement your standard fire insurance policy.

Engaging with an experienced insurance agent can provide personalized insights and recommendations tailored to your unique circumstances. By meticulously choosing the right policy, you can secure not only financial protection but also invaluable peace of mind against the unforeseen devastation of fire.

The Claims Process Explained: Navigating After a Fire

Steps to File a Fire Insurance Claim

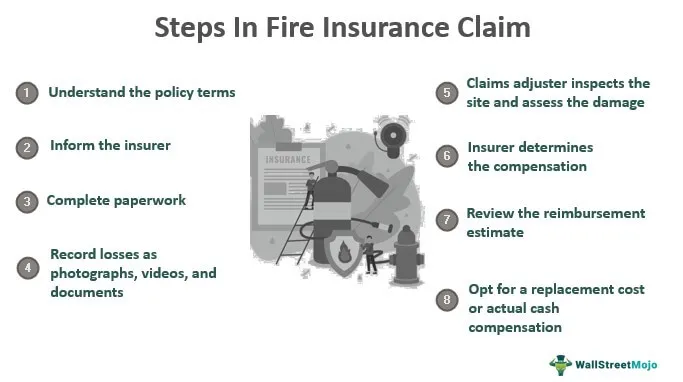

Initiating a standard fire insurance claim can seem overwhelming, but understanding the process can significantly ease the journey. The first step is to notify your insurance provider as soon as possible after the incident. Providing them with all the necessary details of the fire damage is crucial for a smooth process.

- Gather evidence: Take photographs and compile a detailed inventory of all damaged property. This documentation will be invaluable during the claim process.

- Secure the property: To prevent further damage, it’s important to secure your property. This might involve covering broken windows or doors and ensuring the property is safe.

- Contact your insurance company: Inform your insurer about the incident, providing them with initial details and evidence of damage.

- Complete the claim form: Fill out the claim form provided by your insurer with as much detail as possible.

Remember, the key is to communicate effectively with your insurance provider, ensuring they have all the information needed to process your claim.

Understanding the Assessment Process

Once your claim is filed, the insurance company will send an adjuster to assess the fire damage. This step is vital as it determines the extent of the damage and the potential compensation amount. It’s advisable to be present during the assessment to provide additional insights and answer any queries the adjuster might have.

“The adjuster plays a crucial role in determining your claim’s outcome. Be prepared to walk them through the damage and your documentation.”

- Review of evidence: The adjuster will review all documentation and evidence of damage you’ve provided.

- Property inspection: A thorough inspection of the property will be conducted to assess all fire-related damages.

- Claim evaluation: Based on the inspection and documentation, the adjuster will evaluate your claim and determine the compensation amount.

Engaging in this process with patience and providing all requested information promptly will facilitate a smoother and faster claims process.

Receiving Compensation and Rebuilding

After the assessment process concludes and your claim is approved, the next step is receiving compensation. The insurance payout can come in various forms, including direct payment, reimbursement, or payment to contractors. It’s important to understand the terms of your policy to know how compensation will be handled.

“Rebuilding after a fire is not just about repairing structures but recovering your life. Timely compensation plays a significant role in this journey.”

- Review compensation offer: Carefully review the compensation offer from your insurance company to ensure it covers all your losses.

- Complete necessary paperwork: To receive the payout, complete any required paperwork promptly.

- Begin the rebuilding process: With compensation secured, you can start the process of rebuilding your property and life.

The path to recovery after a fire can be long and challenging, but understanding the insurance claim process can ease some burdens. With the right information and a proactive approach, you can navigate through this difficult time more effectively, moving towards rebuilding and recovery with confidence.

Maximizing Your Fire Insurance Coverage: Tips and Strategies

Reviewing Your Policy Annually

One of the most effective ways to ensure that you are fully protected is by conducting an annual review of your fire insurance policy. This ensures that your coverage aligns with any changes in your property’s value or your personal circumstances. For instance, if you’ve made significant improvements to your property, your existing policy might not fully cover these enhancements in the event of a fire.

It’s essential to update your policy to reflect any changes in your property’s value or your personal circumstances to ensure full protection.

Additionally, this annual check-in provides an excellent opportunity to discuss with your insurer any concerns or questions you might have about your coverage. It could also be the perfect time to inquire about any discounts or loyalty programs that could reduce your premiums without compromising on your level of protection.

- Updated Inventory: Keeping a current inventory of your possessions can help in accurately adjusting your coverage needs.

- Discount Qualifications: Ask about new discounts you may now qualify for, such as those for security systems or fire-resistant materials.

- Policy Adjustments: Consider if higher deductibles could lower your premiums, balancing this against the potential out-of-pocket costs in case of a fire.

Remember, the goal is not just to save money but to ensure that your coverage adequately reflects your current situation. Taking proactive steps can lead to both enhanced protection and potential savings on your premiums.

Enhancing Coverage with Add-ons

Maximizing your standard fire insurance coverage often involves looking beyond the basics of your standard policy. Exploring coverage add-ons or endorsements can provide additional protection that a basic policy might not cover. For example, if you’re located in an area prone to wildfires, specific endorsements might be available to cover such risks more comprehensively.

- Extended Replacement Cost Coverage: This add-on can be invaluable, covering beyond your policy’s limit to rebuild your home as it was before the damage.

- Contents Replacement Cost: Ensures that you’ll receive the full cost to replace damaged items, rather than the depreciated value.

- Additional Living Expenses (ALE): Increases the amount available for living expenses if you’re displaced from your home due to a covered loss.

While adding endorsements will likely increase your premium, the additional cost can be far outweighed by the peace of mind and financial security they provide in the event of a fire. It’s about finding the right balance between cost and coverage.

Investing in the right add-ons can significantly enhance your fire insurance protection, providing peace of mind and financial security.

Engaging in a detailed discussion with your insurance provider about available add-ons tailored to your specific needs can reveal opportunities to significantly enhance your coverage. This proactive approach can safeguard against unexpected gaps in protection and ensure comprehensive coverage.

Risk Reduction Measures to Lower Premiums

Implementing risk reduction measures is a proactive strategy to not only enhance the safety of your property but also potentially lower your fire insurance premiums. Insurance companies often offer discounts to policyholders who take steps to reduce their risk of fire damage. This could include installing smoke detectors, fire alarms, or fire-resistant roofing materials. Such improvements demonstrate to insurers that you’re serious about minimizing fire risks.

- Smoke Detectors and Fire Alarms: These are often the first line of defense in preventing extensive fire damage, and insurers may offer discounts for homes well-equipped with these devices.

- Fire-Resistant Materials: Using fire-resistant materials in your home’s construction or during renovations can significantly reduce the risk of fire damage.

- Regular Maintenance: Keeping electrical systems, heating systems, and chimneys in good condition can prevent fires and show insurers that you’re committed to risk reduction.

Additionally, consider joining a Firewise USA® program if available in your area. These programs focus on community efforts to reduce wildfire risks and can further demonstrate to insurers your commitment to fire safety, potentially leading to further discounts.

By taking these steps, not only can you create a safer living environment, but you can also engage in meaningful conversations with your insurer about reducing your premiums. This dual benefit of enhanced safety and cost savings underscores the value of investing in risk reduction measures for your home.

Comparing Fire Insurance Providers: What to Look For

Criteria for Choosing an Insurance Provider

When venturing into the realm of standard fire insurance, the selection of a provider is a decision that warrants careful consideration. The financial stability of an insurance company is paramount. A provider with a solid financial footing assures policyholders of its ability to pay out claims, especially in the aftermath of widespread disasters. Equally important is the range of coverage options offered. Policies should not only cover the structure but also the contents and, if applicable, provide accommodation expenses during repairs.

Understanding the scope of coverage is critical; it determines the breadth of protection in unfortunate events.

- Financial Stability: Research ratings through independent agencies to gauge the insurer’s financial health.

- Scope of Coverage: Assess policies for comprehensive coverage that meets all potential needs.

- Exclusions: Be aware of what the policy does not cover to avoid unexpected surprises during claims.

Moreover, the policy’s deductible is a crucial factor. A higher deductible might lower premiums but increase out-of-pocket costs during a claim. Finally, consider the insurer’s flexibility in policy customization to suit unique needs, ensuring the coverage is tailored precisely to the property’s specifics.

Choosing the right insurer goes beyond mere cost consideration; it’s about ensuring peace of mind with the knowledge that one’s home is well-protected against unforeseeable events. Initiating this selection with a comprehensive evaluation paves the way for a secure and reliable insurance partnership.

Comparing Quotes and Coverage Options

Gathering quotes from various standard fire insurance providers is more than a preliminary step; it’s a strategic move towards securing optimal coverage. The goal is to achieve a balance between affordable premiums and comprehensive coverage. When comparing quotes, it’s crucial to ensure that the basis of comparison is uniform – same coverage levels, deductibles, and add-on options across all quotes.

- Compare Apples to Apples: Ensure the quotes are for comparable coverage to make an accurate comparison.

- Understand the Fine Print: Scrutinize terms and conditions to identify any hidden costs or clauses that could affect claims.

- Check for Discounts: Inquire about discounts for security systems, fire-resistant materials, or multi-policy bundles.

It’s also essential to consider the value-added services some insurers might offer, such as free risk assessments, fire safety advice, or discounts on fire safety equipment. These services can enhance the overall protection of your property and potentially save money in the long run.

“The cheapest quote isn’t always the best. Consider the coverage quality and the insurer’s reputation for a well-rounded decision.”

Engaging in thorough research and quote comparison is an empowering process. It places you in a position of knowledge, enabling a choice that aligns with your specific needs and budget. This approach ensures that when you make your decision, it’s with confidence and clarity.

Customer Service and Claims Satisfaction

The quality of customer service and the efficiency of the claims process are pivotal in choosing a fire insurance provider. An insurer’s responsiveness and support during stressful times, such as after a fire, significantly impact the overall experience. Claims satisfaction ratings and reviews from current and former policyholders offer invaluable insights into a provider’s reliability and customer service ethos.

- Claims Process: Look for an insurer known for a straightforward and quick claims process.

- Customer Support: Evaluate the availability and quality of customer service, especially during emergencies.

- Transparency: Select providers that are clear about their policy terms and claims procedures.

A reputable insurer stands by its policyholders in times of need, ensuring support and guidance through the claims process.

Investigating online forums and speaking directly with current customers can also shed light on real-world experiences with insurers. Additionally, consider the ease of access to customer service, whether through digital platforms or direct contact channels, as this can greatly influence your satisfaction as a policyholder.

Ultimately, selecting a fire insurance provider with a stellar reputation for customer service and claims satisfaction not only secures your investment but also provides peace of mind, knowing that in the event of a disaster, your insurer will be a reliable ally. Embarking on this path with due diligence will lead you to a provider that stands out not just in their offerings but in their commitment to their clients.

Conclusion: Standard fire insurance

Embracing the journey to safeguard your home and peace of mind through standard fire insurance requires a blend of knowledge, vigilance, and proactive decision-making. From understanding what standard fire insurance covers to navigating the intricacies of the claims process, every step you take brings you closer to securing your sanctuary against unforeseen calamities. The importance of reviewing your policy annually, enhancing coverage with thoughtful add-ons, and implementing risk reduction measures cannot be overstated in their collective power to not only lower premiums but also fortify your home’s defense against fire.

Choosing the right insurance provider is a pivotal decision that hinges on comparing quotes, assessing coverage options, and evaluating customer service and claims satisfaction. Armed with the insights from this article, you’re now equipped to make informed choices that align with your needs and values. Remember, standard fire insurance is not just a financial safety net; it’s a commitment to rebuilding and resilience. Let this be your call to action to revisit your policy, explore additional coverage, and take meaningful steps towards protecting your home and loved ones from the unpredictability of fire. Your journey towards optimal fire insurance coverage starts now.

FAQs: Standard fire insurance

What exactly does standard fire insurance cover?

Standard fire insurance typically covers damage to your property and personal belongings caused by fire, including smoke damage, water damage from firefighting efforts, and damages from a lightning strike that leads to a fire. It also often covers living expenses if you’re displaced from your home. However, coverage can vary, so it’s important to review your specific policy details.

Are there any common exclusions in fire insurance policies I should be aware of?

Yes, most fire insurance policies have exclusions. Common exclusions include damage caused by wars, nuclear hazards, and intentional acts by the policyholder. Some policies may also exclude damage from natural disasters like earthquakes or floods unless specific coverage is added. Again, checking your policy for its specific exclusions is crucial.

How can I choose the right fire insurance policy for my needs?

To choose the right standard fire insurance policy, assess the value of your property and belongings to determine the coverage amount you need. Consider any specific risks your home might face, like being in a wildfire-prone area, and look for policies that cover those risks. Compare policies from different providers, focusing on coverage, exclusions, premiums, and deductibles. Consulting with an insurance agent can also provide personalized advice.

What are the steps to file a fire insurance claim?

Immediately after a fire, ensure everyone’s safety and report the fire to the authorities. Then, contact your insurance company to report the claim. Document the damage by taking photos or videos, and make a list of damaged or lost items. Avoid making permanent repairs until the insurance adjuster has assessed the damage. Cooperate with the insurance company’s investigation and assessment process to expedite your claim.

How can I maximize my fire insurance coverage?

To maximize your standard fire insurance coverage, review your policy annually to ensure it reflects current property values and coverage needs. Consider adding endorsements or riders for high-value items or additional risks not covered by the standard policy. Implementing risk reduction measures, like installing smoke detectors and fire-resistant materials, can also help lower your premiums while improving your coverage.

What criteria should I use when comparing fire insurance providers?

When comparing standard fire insurance providers, look at the coverage options, policy limits, and deductibles to ensure they meet your needs. Consider the insurer’s financial stability and reputation to ensure they can meet their obligations. Customer service and claims satisfaction ratings from current policyholders can also provide insight into what you can expect in terms of service. Finally, compare quotes to find the best value for the coverage you need.

Hi, I’m Jack. Your website has become my go-to destination for expert advice and knowledge. Keep up the fantastic work!

I’m really glad to hear that my article helped you feel hopeful!

Thinker Pedia I am truly thankful to the owner of this web site who has shared this fantastic piece of writing at at this place.

I’m really glad to hear that my article helped you feel hopeful!