Navigate the property damage insurance claims process: What to expect process seamlessly. Learn when and how to file a claim, assess damages, and ensure a successful outcome.

Introduction: Property Damage Insurance Claims Process: What To Expect

Embarking on a property damage insurance claims process: What to expect can feel like navigating a maze without a map. Yet, understanding the ins and outs from the get-go can transform this daunting task into a manageable process. This article is your guide through the crucial initial steps, from deciphering your policy coverage to documenting damage and choosing the right contractor for estimates. We’ll also dive into the intricacies of dealing with insurance adjusters, equipping you with strategies to prepare for their visit, negotiate effectively, and understand their role and limitations.

Maximizing your claim settlement is more art than science, requiring insider knowledge and savvy documentation skills. Our tips and strategies will help you avoid common pitfalls and consider when it might be beneficial to hire a public adjuster. Finally, we’ll outline the typical timeline of a claim, from filing to resolution, shedding light on factors that influence processing time and how to set realistic expectations with your insurer. Navigate your property damage insurance claims process: What to expect with confidence, armed with the knowledge from this comprehensive guide.

Navigating the Initial Steps of a Property Damage Insurance Claim

Understanding Your Policy Coverage

Before diving into the complexities of filing a property damage insurance claim, it’s imperative to thoroughly understand your insurance policy coverage. Many policyholders find themselves in challenging situations due to a lack of clarity about what their policies entail. It’s not just about knowing that you have coverage, but understanding the extent of it.

Knowledge of your deductible, coverage limits, and the types of damages covered can significantly influence your claim’s success.

Review your policy documents and look for specific provisions or exclusions that could affect your claim. For instance, water damage might be covered, but if it’s due to flooding, you might need separate flood insurance. This distinction is crucial in preparing your claim.

- Exclusions: Be aware of what your policy does not cover. Knowing these can save you from unexpected disappointments during the claims process.

- Deductibles: Understanding your deductible amount is essential, as it affects the claim payout and your out-of-pocket expenses.

- Coverage Limits: Know the maximum amount your policy will pay for covered damages to manage your expectations and financial planning.

Remember, the more you know about your policy, the better prepared you’ll be to navigate the claims process. Don’t hesitate to contact your insurance agent for clarification on any policy details. This initial step lays the groundwork for a smoother claim experience.

Documenting the Damage Thoroughly

Once you understand your policy coverage, the next critical step is to document the property damage comprehensively. This documentation is vital for your insurance claim, as it provides concrete evidence of the damage and helps justify the claim amount.

- Take detailed photographs: Capture multiple angles and close-ups of the damage to provide a full picture of the extent.

- Make a written account: Complement your photos with a detailed written description of the damage, including dates and times, if possible.

- Keep records of communications: Save all correspondence with your insurance company as part of your claim documentation.

“A picture is worth a thousand words, but together with a comprehensive written description, it becomes an undeniable proof of damage.”

It’s also advisable to not undertake any repairs until after the damage has been fully documented and reported, except for emergency measures to prevent further damage. Document these temporary fixes as well, as they may be reimbursable under your policy.

Effective documentation can significantly expedite the claims process and increase the likelihood of a favorable outcome. It’s about building a strong case for your claim right from the start.

The Importance of Immediate Notification

After ensuring that you and your property are safe, the next indispensable step is to notify your insurance provider about the damage as soon as possible. Prompt notification is not just a procedural formality; it’s a critical element of the claims process that can affect the outcome of your claim.

- Policy requirements: Many policies have specific time frames within which you must report damage. Failing to adhere to these can jeopardize your claim.

- Early assessment: The sooner you report the damage, the quicker an adjuster can assess it, leading to a faster claims process.

- Prevention of further damage: Insurance companies often require that you take reasonable steps to prevent further damage. Early reporting aligns with this requirement.

When notifying your insurer, be prepared to provide a brief overview of the damage. However, avoid making speculative statements about the cause of the damage or the extent. Let the professionals make those determinations.

Remember, the goal of immediate notification is to set the wheels in motion for your claim, ensuring that the process proceeds without unnecessary delays. Your proactive approach can be instrumental in achieving a smoother, more efficient claims process.

Selecting a Reputable Contractor for Estimates

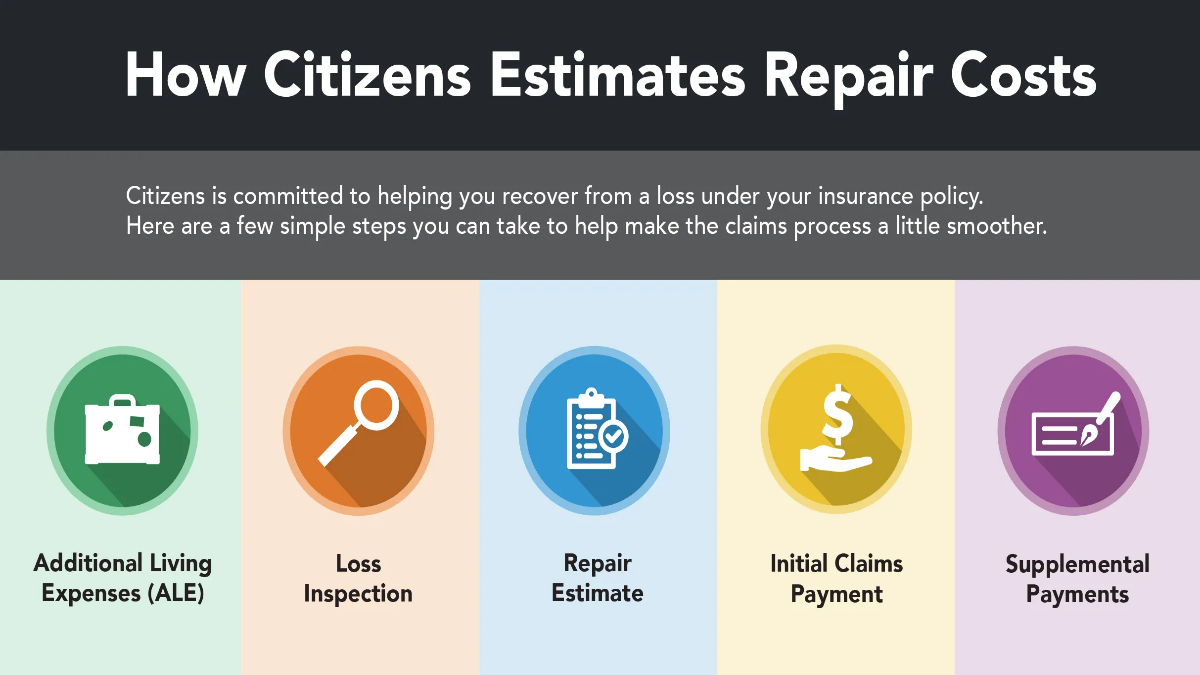

Following the documentation and reporting of your property damage, securing estimates for repairs is a pivotal step. It’s crucial to choose a reputable contractor who can provide a detailed and accurate estimate of the repair costs. This estimate plays a significant role in the insurance claims process, serving as a benchmark for the settlement amount.

- Seek recommendations: Start by asking friends, family, or your insurance agent for contractor recommendations to ensure credibility.

- Verify credentials: Ensure any contractor considered is licensed, insured, and has a solid track record of quality work and integrity.

- Request detailed estimates: An estimate should be itemized and include a comprehensive breakdown of costs for materials and labor.

“A reputable contractor doesn’t just provide a service; they offer peace of mind during the often stressful claims process.”

While it may be tempting to go with the lowest estimate, remember that quality and reliability are paramount. The goal is to restore your property to its pre-damage condition efficiently and effectively, not just cheaply.

Ultimately, a reputable contractor can be a valuable ally in your property damage claim, helping to ensure that the repair estimates are fair, comprehensive, and in line with your policy’s coverage. This careful selection can facilitate a smoother claims process and contribute to a more satisfactory settlement.

Dealing with Insurance Adjusters: What to Expect

Preparing for the Adjuster’s Visit

When an insurance adjuster schedules a visit to assess property damage, it’s crucial to be well-prepared. This preparation not only helps in presenting the damages clearly but also sets the stage for a smooth claim process. Gathering all relevant documentation is a foundational step. This includes receipts, photos of the damage before and after the incident, and any other records that substantiate your claim.

Being organized can significantly impact the adjuster’s assessment and, consequently, the claim resolution.

Moreover, understanding your policy thoroughly will arm you with knowledge about what is covered and what isn’t, allowing you to discuss your claim more effectively. It’s also advisable to have a repair estimate ready, to provide a benchmark for discussions.

Lastly, preparing a list of questions for the adjuster will ensure you don’t forget to address any concerns you might have. This proactive approach not only demonstrates your diligence but also helps in clarifying the process ahead.

Key Information to Provide

- Detailed description of the damage: Providing a comprehensive account of the damages will help the adjuster in evaluating the claim accurately.

- Evidence of the damage: Photos, videos, and any other form of evidence that can visually represent the damage are crucial. They provide indisputable proof of the condition post-incident.

- Documentation of property value and losses: Receipts, previous appraisals, and any other documents that can prove the value of the damaged property and the extent of the loss.

It’s essential to be transparent and thorough when providing information to the adjuster. This not only aids in establishing trust but also ensures that the adjuster has all necessary data to make a fair assessment.

Negotiating the Settlement Offer

Negotiation is a key aspect of the insurance claim process. Once the adjuster presents the settlement offer, it’s important to review it carefully against your own estimates and the policy coverage. If the offer seems low, don’t hesitate to present your calculations and evidence to support your counter-offer.

Effective negotiation is about finding a fair middle ground that reflects the true value of your claim.

- Understand the initial offer: Review the adjuster’s report and the basis of their offer thoroughly.

- Prepare a counteroffer: If necessary, prepare a detailed counteroffer that includes justification for the higher amount requested.

- Communicate effectively: Use clear and concise communication to present your case. Being polite yet firm can greatly influence the negotiation’s outcome.

Remember, the goal of negotiation is to reach an agreement that is satisfactory to both parties. Patience and persistence, backed by solid evidence, are key in achieving a favorable settlement.

Understanding Adjuster’s Role and Limitations

Insurance adjusters play a critical role in the claim process, acting as the bridge between the claimant and the insurance company. They assess the damage, determine the claim’s validity, and negotiate settlements. However, it’s important to recognize that adjusters operate within certain constraints set by their employers.

Adjusters must adhere to the company’s policies and guidelines, which can sometimes limit their flexibility in settlement negotiations. Understanding this dynamic can help set realistic expectations from the outset.

Adjusters are professionals tasked with a challenging role, balancing fairness to claimants with their employer’s guidelines.

Building a cooperative relationship with the adjuster can facilitate a smoother process. While it’s important to advocate for a fair settlement, acknowledging the adjuster’s professional constraints can lead to more productive interactions. By approaching the situation with understanding and preparedness, you position yourself for a more favorable outcome in your property damage claim.

Maximizing Your Claim Settlement: Insider Tips and Strategies

Leveraging Professional Estimates

One of the most critical steps in ensuring you receive the maximum settlement for your property damage claim is to obtain professional estimates. These estimates serve as the foundation of your claim, providing a detailed breakdown of the damages and the associated costs for repair or replacement. It’s not just about having a number to present to your insurance company; it’s about having a documented assessment from a credible source.

Professional estimates can significantly influence the outcome of your claim, making them an indispensable part of the process.

- Choose accredited professionals: Ensure that the estimates are obtained from licensed contractors or repair professionals who are well-regarded in their field.

- Get multiple estimates: This not only provides a range of costs but also a more comprehensive understanding of the damages.

- Detail is key: The more detailed your estimate, the stronger your claim. Each estimate should include a thorough description of the damages, the necessary repairs, and the estimated costs.

Armed with professional estimates, you’re not just presenting numbers to your insurer; you’re presenting a case backed by expert analysis. This not only bolsters your negotiation power but also sets a clear expectation for the settlement you deserve. Remember, the goal here is not just to repair the damage but to restore your property to its pre-loss condition.

The Art of Documentation

Documentation is the cornerstone of a strong insurance claim. From the moment damage occurs, your ability to accurately and comprehensively document the extent and nature of the damage can significantly impact the settlement outcome. This involves taking detailed photographs, maintaining a log of damaged items, and collecting any related receipts or records.

- Photographic evidence: Snap clear, detailed photos from multiple angles to provide a visual account of the damage.

- Inventory of damages: Create a detailed list of damaged items, noting the make, model, and estimated value of each.

- Keep all receipts: This includes receipts for any repairs, replacements, or temporary accommodations, as they can be reimbursed.

Thorough documentation not only supports your claim but also speeds up the claims process.

By systematically documenting every aspect of the damage and your recovery efforts, you transform your claim from a mere request for compensation into a compelling narrative supported by evidence. This narrative is powerful; it not only substantiates your claim but also humanizes it, making it harder for insurers to undervalue your loss.

Avoiding Common Pitfalls

Navigating the insurance claims process can be fraught with potential missteps that can jeopardize your settlement. Being aware of these pitfalls and knowing how to avoid them is essential. One common mistake is underestimating the extent of the damage, leading to inadequate compensation. Similarly, failing to understand the specifics of your insurance policy can result in missed opportunities for coverage.

- Immediate notification: Delaying to inform your insurer about the damage can be detrimental to your claim.

- Overlooking policy details: Every policy has its limitations and exclusions. Knowing these is key to maximizing your claim.

- Accepting the first offer: Initial settlement offers are often lower than what is fair. It’s important to negotiate.

Avoiding these pitfalls requires diligence, attention to detail, and a willingness to advocate for your rights as a policyholder.

By staying informed and proactive throughout the process, you can safeguard your claim from common mistakes that could diminish your settlement. This proactive approach not only maximizes your compensation but also empowers you as a claimant, ensuring that your interests are fully represented and respected.

When to Consider Hiring a Public Adjuster

There are situations in the claims process where enlisting the help of a public adjuster can be particularly beneficial. If the damage to your property is extensive, or if you find yourself overwhelmed by the complexity of the claims process, a public adjuster can serve as your advocate, ensuring that your claim is accurately valued and fairly settled.

- Complex claims: For claims involving significant damage or loss, a public adjuster can navigate the intricate details of filing and negotiation.

- Dispute resolution: If there’s a dispute with your insurer over the value of the claim, a public adjuster can provide expert negotiation.

- Maximizing your settlement: Public adjusters are skilled in identifying overlooked damages that can increase your compensation.

Hiring a public adjuster can make a significant difference in the outcome of your claim, turning a potentially stressful situation into a manageable one.

While there is a cost associated with hiring a public adjuster, the potential increase in your settlement can outweigh this investment. Ultimately, the decision to hire a public adjuster should be based on the complexity of your claim, your comfort level with the claims process, and your desire to ensure you are adequately compensated for your loss. Engaging a public adjuster can be a strategic move to protect your interests and secure the settlement you deserve.

Understanding the Timeline: From Claim Filing to Resolution

Typical Duration of the Claims Process

When you’ve experienced property damage insurance claims process: What to expect and need to file an insurance claim, understanding the typical duration of the claims process is crucial. Generally, the timeline can vary significantly depending on the complexity of the claim and the efficiency of the insurance company. However, most claimants can expect the process to take anywhere from a few weeks to several months.

It’s important to note that straightforward claims might be resolved in under a month, while more complex cases, especially those involving significant property damage or liability issues, might take longer to reach a resolution.

- Initial Assessment: The first step, involving the insurer reviewing your claim, can take a few days to a couple of weeks.

- Adjustment and Investigation: This phase, where the insurer assesses the damage in detail, could extend from a few weeks to a couple of months.

- Resolution: The final stage, which includes the approval and payout, might take an additional few weeks.

Being proactive in submitting all necessary documentation can help expedite this timeline. Remember, each claim is unique, and patience is key.

Factors Influencing Claim Processing Time

- Complexity of the Damage: More severe or complicated damages naturally require a longer assessment period, thus extending the claim process.

- Efficiency of the Claimant: The speed with which you file the claim and provide necessary documentation can significantly affect the processing time.

- Insurance Company’s Workload: The number of claims being handled by your insurer at any given time can also influence how quickly your claim is processed.

Understanding these factors can help manage your expectations and potentially identify areas where you might be able to influence the speed of the process.

“A well-documented claim is a fast-moving claim.” Ensuring you have all your documentation in order can significantly impact the speed of your claim’s resolution.

Keeping open lines of communication with your insurer and promptly responding to requests for information or documentation are also key strategies to avoid unnecessary delays.

Steps to Accelerate the Process

While you may not have control over every aspect of the claims process, there are certain steps you can take to ensure it moves as swiftly as possible. First and foremost, providing complete and accurate information from the start can prevent back-and-forth and reduce processing times. Additionally, understanding your policy in detail means you’ll be better prepared to meet all requirements without delay.

- Detailed Documentation: Keep thorough records and documentation of the damage, including photos and videos, to support your claim.

- Immediate Notification: Notify your insurer as soon as possible after the damage occurs to kickstart the process.

- Professional Estimates: Obtaining professional estimates for repairs can provide a clear framework for the claim amount and expedite approval.

By following these steps, you not only streamline property damage insurance claims process: What to expect the process but also help ensure that your claim is handled with the urgency it deserves. Remember, your goal is to rebuild and recover as quickly as possible, and taking proactive measures can be a significant factor in achieving that outcome.

Setting Realistic Expectations with Your Insurer

Open and honest communication with your insurer is paramount in setting realistic expectations for the duration of the claims process. Discussing the potential timeline and any foreseeable delays at the outset can help mitigate frustration down the line. It’s also beneficial to inquire about any steps you can take to assist in the process, further aligning your expectations with the reality of the situation.

“Understanding is the first step to peace of mind.” By having a clear conversation about the timeline, you’re more likely to feel in control of the process.

- Ask Questions: Don’t hesitate to ask your insurer for updates or clarification on any steps of the process.

- Stay Informed: Keeping yourself informed about the progress of your claim helps manage your expectations and reduces anxiety.

Ultimately, property damage insurance claims process: What to expect process can be lengthy, knowing what to expect and how to actively participate can make it feel more manageable. Your insurer is your ally in this journey, and working together towards a resolution is in both of your best interests.

Conclusion: Property Damage Insurance Claims Process: What To Expect

Navigating through the complexities of a property damage insurance claims process: What to expect can indeed be a daunting journey. Yet, understanding the essence of your policy, coupled with meticulous documentation and prompt communication, paves the way for a smoother process. The significance of engaging with reputable contractors and being well-prepared for the insurance adjuster’s visit cannot be overstated. Furthermore, mastering the art of negotiation and leveraging insider tips can substantially influence your claim’s outcome. It’s crucial, however, to remember the timeline from claim filing to resolution, setting realistic expectations with your insurer while avoiding common pitfalls that could delay your claim.

This journey, though challenging, offers an invaluable opportunity to learn and better prepare for unforeseen future incidents. We encourage you to delve deeper into each discussed strategy, fortifying your knowledge and readiness. Whether it’s refining your understanding of policy coverage, enhancing your negotiation skills, or considering the engagement of a public adjuster, every step you take is a stride towards safeguarding your property’s value and your peace of mind. Let this guide be your beacon, illuminating the path to a maximized claim settlement and a swift, satisfactory resolution.

FAQs: Property Damage Insurance Claims Process: What To Expect

What should I first do after experiencing property damage?

Immediately after experiencing property damage, it’s crucial to understand your insurance policy coverage. Document the damage thoroughly by taking pictures or videos. Then, notify your insurance provider as soon as possible to initiate the claim process. It’s also advisable to contact a reputable contractor to get an estimate for the repairs needed.

How should I prepare for the insurance adjuster’s visit?

Prepare for the adjuster’s visit by compiling a detailed inventory of all damaged property, including descriptions, the date of purchase, and the cost of these items. Ensure you have all your documentation ready, such as photos or videos of the damage, and any receipts for repairs or replacements already made. Be ready to point out all areas of concern during the adjuster’s walkthrough.

What are some tips for negotiating my settlement offer?

To effectively negotiate your settlement offer, leverage professional estimates you’ve obtained to justify the amount you believe is fair. Understand the details and limits of your policy to argue your case effectively. Documentation is key, so ensure all damage and correspondence with the insurance company are well-documented. If negotiations stall, consider seeking the advice or representation of a public adjuster or attorney.

How can I maximize my claim settlement?

Maximizing your claim settlement involves leveraging detailed professional repair estimates, thoroughly documenting all damages and interactions with your insurer, and avoiding common pitfalls such as underreporting damages or waiting too long to file a claim. In some cases, hiring a public adjuster can provide additional expertise in negotiating with your insurance company.

What factors influence the processing time of my claim?

The processing time of your claim can be influenced by several factors, including the complexity and severity of the damage, the workload of the adjuster, the completeness and accuracy of your claim submission, and the efficiency of communication between all parties involved. External factors such as natural disasters can also impact processing times due to an increased volume of claims.

How long does the property damage insurance claim process usually take?

The duration of the claims process can vary significantly but typically takes anywhere from a few weeks to several months. This timeline can be affected by the complexity of the claim, the promptness of your reporting and documentation, and the insurer’s efficiency in processing claims. To accelerate the process, ensure timely and thorough communication with your insurer, and provide all required documentation as quickly as possible.

insurance | Insurance for High-Net-Worth Individuals: High-net-worth individuals often require more specialized insurance solutions. MAFA Insurance works with clients to develop tailored policies that protect their unique assets and liabilities.

I’m really glad to hear that my article helped you feel hopeful!