What can you claim on house insurance? Embarking on the journey of homeownership brings its share of joys and challenges, with one of the most pivotal aspects being the proper understanding and managing of your home insurance coverage. This guide demystifies the complexities of home insurance, from the essential types of coverage and exclusions you can’t afford to overlook, to calculating your needs and ensuring your assets are adequately protected. Whether you’re navigating the aftermath of a weather calamity, safeguarding against theft, or ensuring you’re covered for liability and living expenses, we’ve got you covered.

Dive into the intricacies of maximizing your claims post-incident, steering clear of common filing pitfalls, and the vital steps to take immediately after an unforeseen event. Additionally, uncover the significance of regularly reviewing and adjusting your policy in response to life’s inevitable changes. With practical tips and expert insights, this article empowers you to make informed decisions, ensuring your home insurance works hard for you.

Understanding What can you claim on house insurance?

Types of Coverage: What’s Included?

Understanding the breadth of What can you claim on house insurance? coverage is essential for every homeowner and renter. At its core, home insurance provides protection against various unforeseen events, but the extent can vary significantly. Standard policies typically encompass damages caused by fire, theft, and certain natural disasters. However, the specifics can differ based on your insurer and the plan you choose.

Remember, not all home insurance policies are created equal. It’s imperative to know exactly what yours covers.

- Dwelling Coverage: This fundamental aspect covers the physical structure of your home, including walls and roofs.

- Personal Property: This covers belongings within your home, such as furniture and electronics, against theft or damage.

- Liability Protection: In case someone is injured on your property, this coverage can help with legal expenses and damages.

Exploring the specifics of these coverages with your insurance provider can illuminate the nuances of your policy, ensuring you understand the protection you’re entitled to.

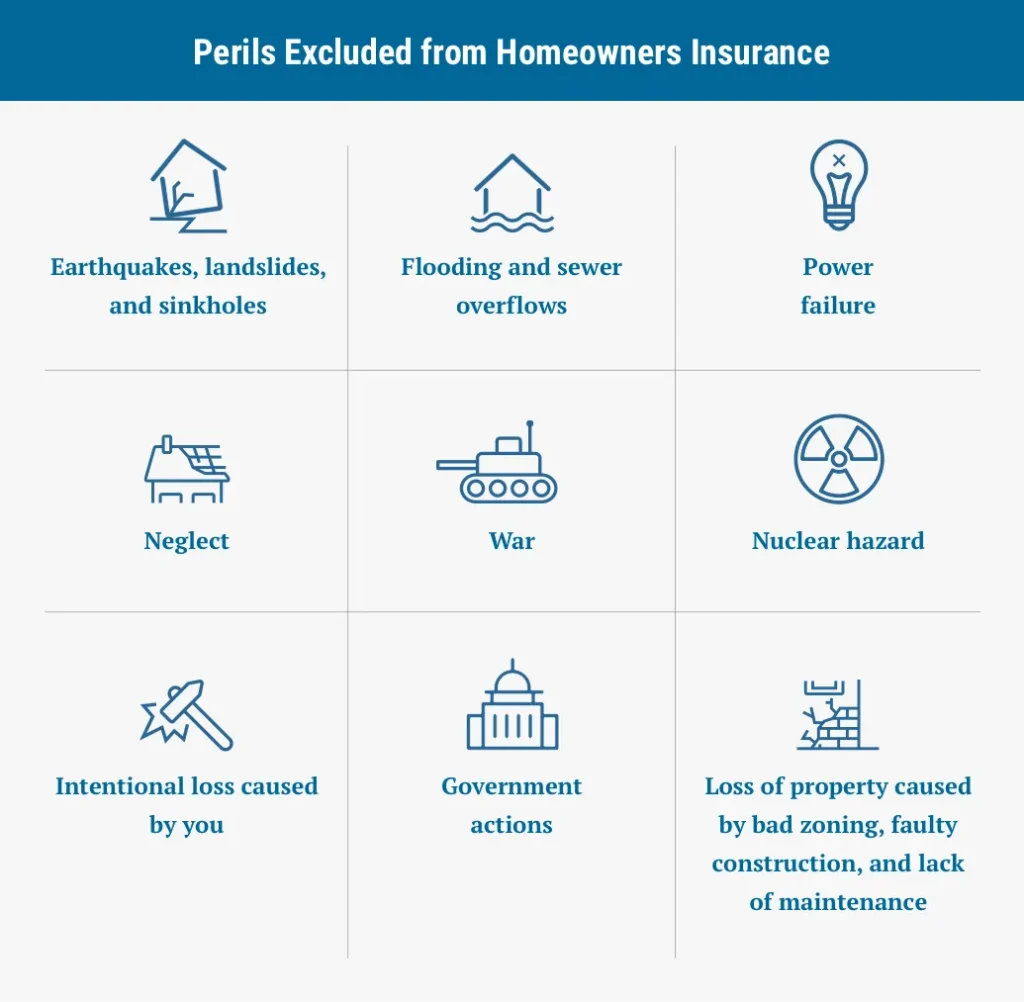

The Fine Print: Exclusions You Need to Know

While home insurance offers extensive protection, it’s crucial to be aware of the exclusions within your policy. Certain disasters, like floods and earthquakes, are commonly not covered under standard policies. This can be a significant oversight for those residing in prone areas.

- Floods: Typically requires separate insurance.

- Earthquakes: Also often necessitates an additional policy.

- Regular Wear and Tear: Damage from aging and normal use is not covered.

Understanding these exclusions is essential. It empowers homeowners and renters to seek additional coverage if their current policy leaves gaps in protection.

“Assumptions can be costly. Always verify what your home insurance does not cover.”

Calculating Your Coverage Needs

Determining the right amount of home insurance coverage is a balancing act. Too little may leave you vulnerable in a disaster, while too much could mean overpaying for protection you don’t need. Start by assessing the replacement cost of your home, not its market value. This estimate should reflect the cost to rebuild your home at current prices.

- Inventory Your Belongings: A detailed list helps in assessing the coverage needed for personal property.

- Consider Liability Needs: If you frequently host guests, higher liability coverage may be prudent.

- Special Coverage for Valuables: High-value items may require additional protection beyond standard policy limits.

Engaging with an insurance professional to review your specific circumstances can guide you towards adequate coverage that aligns with your needs and budget.

What can you claim on house insurance? Tips for Ensuring Adequate Protection

To ensure your home insurance policy provides adequate protection, regular reviews and updates are critical. Changes in your home, such as renovations or the acquisition of valuable items, can alter your coverage needs. Additionally, staying informed about the latest in home insurance trends and policy offerings can reveal opportunities for better rates or more comprehensive coverage.

“Your home’s insurance needs can evolve. Annual reviews keep your coverage aligned with your current situation.”

- Annual Policy Review: Adjust your coverage as your home and possessions change.

- Shop Around: Comparing policies can uncover better deals or more suitable coverage options.

- Understand Policy Limits and Deductibles: Knowing these can help you make informed decisions about the coverage you choose.

Proactively managing your home insurance ensures that you’re always adequately protected, providing peace of mind in knowing that you’re prepared for whatever comes your way.

The Most Common Claims on Home Insurance

Weather-Related Damage: From Storms to Floods

When the skies darken and the winds howl, homeowners know all too well the potential for weather-related damage that can ensue. From the furious onslaught of hurricanes to the silent threat of heavy snowfalls, nature’s fury is a common catalyst for filing home insurance claims. These incidents not only cause structural damage but can also lead to secondary issues like water damage and mold.

“The wrath of nature holds no bounds, making weather-related claims one of the most common reasons homeowners reach out to their insurance providers.”

- Hurricanes and Tornadoes: These powerful storms can rip roofs off homes, shatter windows, and uproot trees, leading to significant property damage.

- Heavy Snowfall: The weight of accumulated snow can cause roofs to collapse, resulting in costly repairs.

- Floods: Often a consequence of hurricanes or heavy rains, floods can infiltrate homes, ruining floors, walls, and personal belongings.

Understanding the coverage terms for these natural disasters is crucial for homeowners. While standard policies cover a range of weather-related damages, some, like floods, often require additional coverage. Preparing your home to withstand these events and knowing your policy’s specifics can mitigate the financial impact.

Theft and Vandalism: Protecting Your Belongings

- Break-ins: A common claim, break-ins can leave homeowners with not only lost valuables but also the need for repairs to doors, windows, and locks.

- Vandalism: Acts of vandalism, such as graffiti or broken windows, can damage a home’s aesthetics and structural integrity.

- Theft: Beyond the physical premises, theft of outdoor items like bikes or grills is also a frequent insurance claim.

The emotional and financial toll of theft and vandalism on a family can be significant. Home insurance offers a safety net, covering the loss of personal items and the cost of repairs. Enhancing home security with alarms, cameras, and strong locks can deter criminals and potentially lower insurance premiums.

“A secured home is not only a deterrent to thieves but also a step towards peace of mind for homeowners.”

Reviewing your policy’s coverage limits and ensuring valuable items are adequately covered is essential. In the unfortunate event of theft or vandalism, having an inventory of your belongings can streamline the claims process.

Liability Coverage: When Others Are Injured on Your Property

Homeownership comes with the responsibility of ensuring the safety of those who enter your property. Whether it’s a guest tripping over a rug or a neighbor’s child getting injured while playing in your yard, liability coverage is a critical component of homeowner’s insurance. It protects homeowners against claims for bodily injury or property damage for which the homeowner is found legally responsible.

- Bodily Injury: Covers medical bills, lost wages, and legal costs if someone is injured on your property and you’re deemed responsible.

- Property Damage: Helps cover the cost of repairs if you or a family member damages another person’s property.

- Legal Costs: Provides coverage for legal expenses if you’re sued over an accident that occurred on your property.

“Liability coverage is your safeguard against the unforeseen, ensuring that an accident on your property doesn’t lead to financial ruin.”

Enhancing safety measures around your home, such as securing swimming pools and fixing loose railings, can prevent accidents and reduce the likelihood of liability claims. Familiarizing yourself with the specifics of your liability coverage can also prepare you for any potential incidents.

Living Expenses: Coverage When Displaced from Your Home

In the aftermath of a disaster that renders your home uninhabitable, the living expenses coverage in your home insurance policy becomes a lifeline. This coverage, often referred to as Additional Living Expenses (ALE), provides for the costs of living away from home if you cannot live in your house due to an insured disaster.

- Hotel Bills: Covers the cost of hotel stays during the repair or rebuilding of your home.

- Meals: Reimburses for meals when you don’t have access to your kitchen.

- Storage Fees: Covers the cost of storing your belongings if your home is damaged or being repaired.

Understanding the specifics of your ALE coverage is crucial. Policies can vary in terms of what’s covered and for how long. Keeping receipts and maintaining clear communication with your insurance provider can ensure you fully utilize this coverage.

“Being displaced from your home is challenging, but having comprehensive living expenses coverage can ease the financial and emotional strain.”

While no one anticipates having to leave their home, knowing that your insurance policy includes coverage for additional living expenses can provide peace of mind during turbulent times. Preparing an emergency plan and familiarizing yourself with your policy’s details can make all the difference.

Maximizing Your Claim: Steps to Take After an Incident

Immediate Actions Post-Incident

When an incident occurs, the initial steps you take can significantly impact the outcome of your insurance claim. Firstly, ensure that everyone is safe and that it’s secure to remain on the property. Then, promptly report the incident to the authorities if necessary, as their reports can serve as crucial evidence for your claim.

Immediate reporting not only facilitates a smoother claim process but also helps in documenting the incident accurately.

After ensuring safety and reporting, begin mitigating further damage to your property. This might include temporary repairs or measures to prevent additional losses. Remember, insurance policies often require that you take reasonable steps to minimize further damage.

- Documenting initial damage: Take photographs or videos of the damage before any temporary repairs are made.

- Contacting your insurance company: Notify your insurer as soon as possible to get the claim process started.

- Securing property: If possible, secure your property from further damage or theft.

Maintaining a calm and proactive approach during these initial moments can set a positive tone for the entire claim process, ensuring that you’ve taken all the necessary steps to protect your property and lay a solid foundation for your claim.

Documenting Damage for Your Claim

- Comprehensive documentation: Start by creating a detailed list of damaged or lost items. Include descriptions, purchase dates, and approximate values to make your claim stronger.

- Photographic evidence: Take clear photos or videos of all damages. This visual evidence is compelling when filing your claim.

- Keep damaged items: If safe, keep damaged items until the insurance adjuster has reviewed them. This serves as physical proof of your claim.

Effective documentation is a critical step in maximizing your insurance claim. It provides your insurer with a clear picture of the incident’s impact, making it easier for them to assess your losses accurately.

Remember, the more evidence you provide, the less room there is for dispute over the extent of the damages.

Additionally, compile any relevant receipts, warranties, or manuals that can support your claim. These documents can significantly enhance the credibility of your claim, potentially leading to a higher payout.

Finally, ensure all communication with your insurance company is documented. Keep records of emails, letters, and phone calls to maintain a clear trail of your claim’s progress.

Navigating What can you claim on house insurance? the Claims Process

The journey through What can you claim on house insurance? claims process can be complex, but understanding the steps can make it more manageable. Initially, you’ll need to file your claim promptly. Delaying this step can result in complications or denials. Provide your insurer with all the necessary documentation to expedite the process.

Following the claim filing, an insurance adjuster will be assigned to assess the damage. It’s crucial to be present during their visit to ensure they fully comprehend the extent of the damage. Politely point out all areas of concern and provide them with copies of your documentation.

Cooperating fully with the insurance adjuster can positively influence the outcome of your claim.

Understanding your policy is equally important. Know what is covered and what is not to set realistic expectations regarding your claim’s outcome. If you disagree with the adjuster’s assessment, you are entitled to get a second opinion or hire a public adjuster to negotiate on your behalf.

- Review your policy: Understanding your coverage is crucial for a smooth claims process.

- Stay organized: Keep detailed records of all interactions and submissions to your insurance company.

- Ask questions: Don’t hesitate to seek clarification on any doubts you may have during the process.

Staying informed and involved throughout the process can significantly influence the speed and outcome of your claim, leading to a more favorable settlement.

Avoiding Common Pitfalls in Claim Filing

To ensure a smooth claim filing process, it’s essential to be aware of common pitfalls and actively work to avoid them. One major mistake is underestimating the value of your claim. Ensure you have accurately assessed the damage and its impact to avoid receiving less than what you’re entitled to.

Another pitfall is failing to keep adequate records of your possessions and their value before an incident occurs. This proactive step can make the claims process smoother and more straightforward. Additionally, neglecting to read and understand your insurance policy thoroughly can lead to surprises about what is and isn’t covered.

Being prepared and knowledgeable about your policy and rights can empower you to navigate the claims process more effectively.

Avoiding hasty decisions is also crucial. Don’t rush into agreements or repairs without consulting your insurance provider, as this may affect your claim. Patience and diligence are key to ensuring you’re fully compensated for your losses.

- Meticulous documentation: Keep a thorough record of all damages, communications, and transactions related to your claim.

- Understanding your policy: A deep understanding of your policy’s coverage can prevent unexpected disappointments.

- Professional advice: Consider seeking advice from legal or claims professionals if you’re unsure about any aspect of your claim.

By being vigilant and prepared, you can navigate the claims process more smoothly and maximize your potential payout, ensuring a quicker and more satisfactory resolution to an otherwise stressful situation.

When to Review and Adjust Your Home Insurance Policy

Life Changes that Impact Your Coverage Needs

When significant life events occur, they often necessitate a reassessment of your home insurance needs. Whether it’s a marriage, the birth of a child, retirement, or acquiring expensive personal items, each of these milestones might alter the risk profile of your household.

- Marriage or Divorce: Combining households or dividing assets can significantly change your coverage requirements.

- Home Renovation: Upgrades can increase your home’s value, requiring more comprehensive coverage.

- New Family Members: The addition of dependents may necessitate increased personal property coverage.

- Acquiring Valuable Items: Purchasing expensive jewelry or electronics can exceed your policy’s standard personal property limits.

Adjusting your policy in response to these life changes ensures that you’re neither overpaying for unnecessary coverage nor underinsured in the event of a claim. Regularly reviewing your policy allows you to adapt to these changes smoothly, ensuring your coverage meets your current needs.

Remember, insurance is designed to provide peace of mind. Keeping your policy aligned with your life’s current trajectory is essential for maintaining that security. Don’t wait for a claim to discover you’re inadequately covered. Proactively manage your home insurance to reflect your life’s ongoing evolution.

The Benefits of an Annual Insurance Review

- Ensuring Adequate Coverage: Regular reviews help confirm that your policy’s coverage limits are sufficient, considering any changes in your home’s value or personal possessions.

- Identifying Discounts: You might be eligible for new discounts that can lower your premiums, such as security system installations or fire prevention measures.

- Adjusting for Market Changes: Economic fluctuations can affect property values and replacement costs, potentially necessitating policy adjustments.

- Personalizing Coverage: Life changes may require additional riders or endorsements to fully protect new assets or cover specific risks.

Conducting an annual review of your home insurance policy with your agent can lead to significant benefits, including potential savings and improved coverage. It’s an opportunity to ask questions, clarify coverage details, and make informed decisions about your policy.

“An ounce of prevention is worth a pound of cure.” This adage holds especially true for home insurance, where an annual review can preempt financial strain by ensuring your coverage is up-to-date.

This proactive approach can spare you from the distress of discovering gaps in your coverage when it’s too late. Engage in an annual review and rest easy knowing your home insurance policy is working as hard as it can to protect you and your assets.

Upgrading Your Policy: What to Consider

Deciding to upgrade your home insurance policy is a significant step that involves several considerations. The goal is to ensure your coverage matches the current value of your home and possessions, protecting you against potential losses.

Understanding the distinction between market value and replacement cost is crucial when upgrading your policy. The former relates to your home’s current purchase price, while the latter covers the cost to rebuild your home as it was.

- Assessing Coverage Limits: Verify that your policy’s limits reflect the true cost of rebuilding your home and replacing its contents.

- Reviewing Deductibles: Consider whether adjusting your deductible makes sense for your financial situation, potentially lowering your premium.

- Evaluating Additional Coverage: Explore options like flood or earthquake insurance, particularly if your area is prone to these disasters.

- Understanding Policy Exclusions: Be aware of what your policy does not cover and consider endorsements to fill those gaps.

Upgrading your policy can be a balancing act between enhancing coverage and managing costs. It’s essential to work closely with your insurance agent to tailor your policy to your specific needs, ensuring you have comprehensive protection without overpaying.

Regularly revisit and refine your coverage. As your life evolves, so too should your home insurance policy. By staying proactive, you can safeguard your home and peace of mind against the unexpected.

Communicating with Your Insurance Agent: Tips for Success

Effective communication with your insurance agent is the cornerstone of maintaining an insurance policy that accurately reflects your needs. It’s not just about updating them on life changes; it’s about building a relationship where your coverage is continually optimized for your situation.

“A good conversation is as stimulating as black coffee, and just as hard to sleep after.” Similarly, engaging discussions with your insurance agent can energize your policy, keeping it robust and relevant.

Here are ways to ensure successful interactions:

- Prepare for Meetings: Before meeting your agent, compile a list of questions and concerns. Include any significant life changes, questions about coverage, or clarification on policy features.

- Review Your Policy Annually: Make it a habit to sit down with your agent once a year to review your policy in detail. This ensures your coverage remains aligned with your needs.

- Be Open and Honest: Share complete and accurate information about your property and lifestyle. Omissions or inaccuracies can lead to gaps in coverage.

- Ask for Customization: Inquire about tailoring your policy with endorsements or riders that address specific concerns or valuable items.

Remember, your insurance agent is your ally in navigating the complexities of home insurance. By fostering open communication, you can ensure your policy evolves in tandem with your life, offering protection that mirrors your current circumstances.

Take the initiative to reach out and engage with your agent regularly. This proactive approach can make all the difference in keeping your home insurance policy not only adequate but optimized for your peace of mind.

Conclusion: What can you claim on house insurance?

Embarking on the journey of understanding what can you claim on house insurance? coverage equips you with the knowledge to protect your most valuable asset against the unforeseeable. From dissecting the layers of coverage that safeguard your dwelling against weather-related damage and theft, to navigating the intricacies of liability coverage and living expenses support, the essence of insurance is not just in the policy details but in the peace of mind it affords.

Recognizing the pivotal steps to maximize your claim post-incident, and the importance of regularly reviewing and adjusting your policy in response to life’s inevitable changes, underscores the dynamic nature of home insurance. As you move forward, let the insights garnered serve as a beacon, guiding you to engage in meaningful conversations with your insurance agent, ensuring your home remains a sanctuary against storms, both literal and metaphorical. Embrace this knowledge, and take proactive steps towards fortifying your home’s defense against the unexpected, making it not just a place of residence, but a secure haven for your future.

FAQs: What can you claim on house insurance?

What types of coverage are included in a standard home insurance policy?

Standard home insurance policies typically include coverage for the structure of your home, personal belongings, liability protection, and additional living expenses if you’re displaced from your home due to a covered incident. Specific inclusions can vary, so it’s important to review your policy details or consult with your insurance agent.

Are there common exclusions I should be aware of in my home insurance policy?

Yes, most home insurance policies have exclusions that you need to be aware of. Common exclusions include damage from floods, earthquakes, routine wear and tear, and intentional damage. It’s crucial to read the fine print of your policy and consider additional coverages if needed.

How do I calculate how much coverage I need for my home?

To calculate your coverage needs, consider the cost to rebuild your home at current market rates, the value of your personal belongings, and your liability exposure. Working with an insurance agent can help you accurately assess and ensure you have adequate protection for your specific situation.

What are the most common claims made on home insurance policies?

The most common claims on home insurance include weather-related damage (like storms and floods), theft and vandalism, liability claims when others are injured on your property, and coverage for living expenses if you’re displaced from your home. It’s important to understand your policy’s coverage in these areas.

What steps should I take immediately after an incident to maximize my insurance claim?

Immediately after an incident, ensure safety first, then document the damage with photos or videos, report the incident to your insurance company as soon as possible, and keep records of any temporary repairs or expenses. These steps can help streamline the claims process and ensure you receive adequate compensation.

When should I review and adjust my home insurance policy?

It’s wise to review and potentially adjust your home insurance policy annually, or after significant life changes like a major purchase, home renovation, or a change in marital status. Regular reviews ensure your coverage keeps pace with your changing needs and provides the opportunity to discuss updates with your insurance agent.