Facing a Reasons Insurance Companies Deny Fire Claims? Discover the top reasons insurance companies might deny your fire claim and learn how to effectively navigate the claims process.

Introduction: Reasons Insurance Companies Deny Fire Claims

When disaster strikes in the form of a fire, you expect your insurance to be the safety net that helps you rebuild and recover. However, not all claims proceed smoothly. Understanding the top reasons your insurance company may deny your fire claim is crucial for any homeowner in the US. This knowledge can prepare you to file your claim effectively and contest any denials that may come your way.

1. Lack of Coverage or Insufficient Coverage:

One of the primary reasons for a fire claim [Reasons Insurance Companies Deny Fire Claims] denial is the lack of appropriate coverage. Many policyholders are not fully aware of their policy’s specifics until they file a claim. For instance, certain types of fire damages might not be covered, or your policy limit may not be sufficient to cover the extent of the damage.

2. Arson or Fraudulent Claims:

Insurance companies meticulously investigate fire claims to rule out arson or fraud. If an investigation concludes that the fire was intentionally set by the policyholder or if there’s any discrepancy in the claim details, the claim will be denied [Reasons Insurance Companies Deny Fire Claims].

3. Late Claim Submission:

Timeliness is key when filing any insurance claim. Most policies have strict deadlines for when a claim can be filed following an incident. Failing to submit your claim within this period can result in denial.

4. Non-Payment of Premiums:

An insurance policy is a contract that requires the policyholder to pay premiums on time. If your policy lapsed due to non-payment at the time of the fire, your insurance company would likely deny your claim.

5. Unreported Renovations or Improvements:

If you’ve made significant renovations or improvements to your property without notifying your insurance company, this can affect the value of your claim. In some cases, failure to report these changes can lead to a claim denial because the policy does not reflect the property’s true value at the time of loss.

6. Exclusions Specified in Your Policy:

Every insurance policy has exclusions. Common exclusions that might affect fire claims include damages caused by wars, nuclear hazards, or specific natural disasters. Reviewing your policy’s exclusions section is vital to understand what is not covered.

7. Failure to Mitigate Further Damage:

After a fire, policyholders are expected to take reasonable steps to prevent further damage to the property. This could include covering broken windows or turning off the water to prevent flooding. Failure to do so might result in a partial or total denial of your claim [Reasons Insurance Companies Deny Fire Claims].

Insurance Companies May Deny Your Fire Claim?

Insurance companies scrutinize claims to ensure they meet policy conditions. Common reasons for denial include late claim submissions, lapsed policies due to non-payment of premiums, and failure to mitigate further damage. Fraudulent claims or suspicions of arson are also significant factors.

Conditions for Fire Insurance Claim:

To file a successful fire insurance claim, you must promptly notify your insurer, document the damage extensively, and submit a detailed claim form. Cooperation with the insurance adjuster’s investigation and adherence to policy deadlines are also critical.

Exclusions of Fire Insurance:

Fire insurance policies typically exclude damages caused by wars, nuclear hazards, and sometimes, natural disasters. Another common exclusion is arson; intentional fires set by the policyholder are not covered.

On What Grounds Can an Insurance Claim Be Rejected?

Claims can be rejected on grounds such as misrepresentation or non-disclosure of material facts, violation of policy terms, and damages falling under policy exclusions.

Limitations of Fire Insurance:

Fire insurance limitations often involve coverage caps that may not fully cover the loss, especially if significant improvements to the property were not reported to the insurer. Time limits for filing claims and specific exclusions also limit coverage.

Rules of Fire Insurance:

The principle of indemnity is a fundamental rule, meaning the policyholder should not profit from a claim but rather be restored to the pre-loss condition. Insurable interest, utmost good faith, and subrogation are also key principles guiding fire insurance.

What to Do if Insurance Company Denies Your Claim?

First, review the denial letter for the specific reasons for rejection. You can then submit a written appeal with additional documentation and evidence supporting your claim.

How Do You Fight an Insurance Claim Rejection?

Fighting a rejection involves gathering detailed documentation, seeking an independent appraisal, consulting with a public adjuster, or obtaining legal advice to challenge the insurer’s decision.

Section 45 of the Insurance Act:

Section 45 of the Insurance Act protects policyholders from claim denial after three years on the grounds of misrepresentation or nondisclosure unless the insurer proves fraudulent intent.

12 Perils of Fire Insurance:

Common perils include lightning, explosion, riots, strikes, aircraft damage, malicious damage, storm, flood, bursting or overflowing of water tanks, theft during or after the fire, and impact damage.

Fire Insurance Subject to:

Fire insurance policies are subject to policy terms, which define covered perils, exclusions, conditions for filing claims, and the process for dispute resolution.

Claim Payout Timeline:

The timeline for insurance payout after a fire varies but typically ranges from a few weeks to several months, depending on the claim’s complexity and the insurer’s efficiency.

California-Specific Denial Reasons:

In California, common reasons for fire claim denials include areas prone to wildfires not being covered or insufficient documentation proving the extent of damages.

Dealing with Insurance Adjusters:

Maintain open communication, provide all requested documentation, and consider hiring a public adjuster if negotiations stall or you feel the settlement offer is too low.

Reasons Insurance Companies Drop You:

Non-renewal or cancellation can occur due to increased risk, filing too many claims, or significant changes to the insured property that increase risk.

House Fire Insurance Payout:

Payouts are based on the policy’s terms, covering either the replacement cost or the actual cash value of the lost property, minus any deductible.

Mercury Insurance House Fire Claim Denied:

Specific cases like a denied claim from Mercury Insurance should be addressed by reviewing the denial reasons, consulting with the insurer, and possibly seeking legal advice.

Arson Not Covered:

Arson committed by the policyholder or with their knowledge is not covered due to the illegal intent behind the act.

Insurance Refusal for Forest Fire:

Insurers may refuse claims if they determine the property was in a high-risk area for forest fires not covered by the policy.

Immediate Steps Post-Fire: Filing Your Home Insurance Claim

The moments after a fire are crucial. Once it’s safe and the flames are extinguished, your first action should be to contact your home insurance agent. Filing your claim as soon as possible is critical for a few reasons:

- Speeds up the recovery process: Prompt filing means quicker assessment and reimbursement, helping you recover sooner.

- Minimizes claim backlog: Especially in areas affected by widespread fires, early filing can prevent your claim from being at the bottom of a long list.

Essential Information for Your Claim:

- Damage type

- Incident date

- Any injuries incurred

- Detailed damage description

- Necessary temporary repairs undertaken

- A police report if available

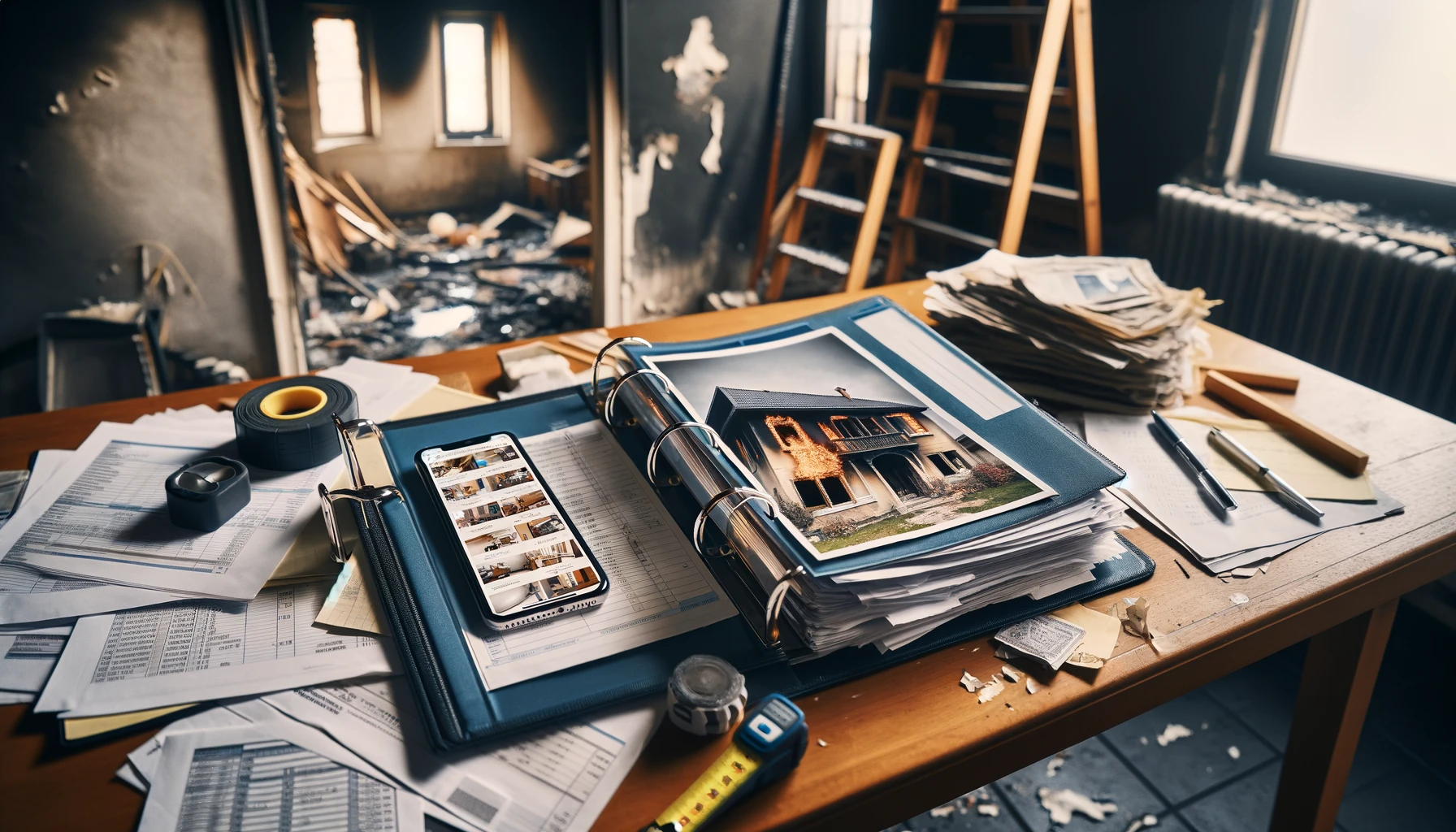

Documenting Damages: Reasons Insurance Companies Deny Fire Claims

A Step-By-Step Approach Documenting the extent of the damage thoroughly is crucial. Here’s how to ensure nothing is overlooked:

- Photograph everything: From large structural damages to personal belongings.

- Keep a detailed record: Use a binder to organize photos, receipts, and communications with your insurer.

- Leverage digital tools: Your phone and social media can be goldmines for pre-fire images of your home.

Securing Your Property Post-Fire

After a fire, securing your property from further damage is both a necessity and a responsibility. This includes:

- Boarding up broken windows

- Covering roof damage with tarps

- Keeping receipts for any emergency repairs for insurance reimbursement

Engaging With Your Insurance Adjuster

The insurance adjuster is your main point of contact with your insurance company. Here’s how to interact effectively:

- Be present during assessments: Guide them through the damage for an accurate evaluation.

- Communicate clearly and assertively: You know your home best. Ensure the adjuster is aware of all damages, visible and hidden.

- Maintain politeness: Respectful communication can make the process smoother for everyone involved.

Understanding Your Insurance Coverage

Knowledge of your policy specifics can significantly affect your claim’s success. Familiarize yourself with:

- Dwelling coverage (Coverage A)

- Other structures (Coverage B)

- Personal property (Coverage C)

- Additional living expenses (Coverage D)

Managing Living Expenses

If you’re displaced, meticulously track all related expenses. Your policy’s Coverage D may reimburse you for costs like hotel stays and meals out.

Choosing the Right Contractor

Insurance won’t cover shoddy repair work. It’s your right to choose your contractor:

- Do thorough research: Compare quotes and check reviews.

- Verify licenses: Ensure your contractor is qualified and reputable.

Advancing Your Claim

In immediate need of funds? Don’t hesitate to request an advance on your claim from your insurance provider. This can provide necessary financial relief but remember it’s deducted from the final payout.

Legal Support: Reasons Insurance Companies Deny Fire Claims

- Negotiations stall: A lawyer can advocate on your behalf.

- Wildfire involvement: If a third party’s negligence caused the fire, legal support could help you seek compensation beyond your insurance claim.

When to Consider It The complexity of fire insurance claims can sometimes necessitate legal advice or representation. This is especially true in cases where:

- Insurance Payouts: Following an adjuster’s assessment, your insurer will offer a settlement to cover repairs and temporary relocation costs.

- Smoke Damage Claims: You can claim for a wide range of smoke-damaged items, from personal belongings to structural damage.

- Maximizing Your Claim: Understanding your policy, documenting everything, and resisting pressure for quick settlements are key to maximizing your fire insurance claim benefits.

Conclusion: Reasons Insurance Companies Deny Fire Claims

Navigating fire insurance claims requires understanding the intricate details of your policy, the reasons behind claim denials, and the conditions under which claims are accepted or rejected. Armed with this knowledge and by following the correct procedures, you can better manage the claims process and contest denials when necessary. If you encounter obstacles, consulting with professionals can provide the support needed to navigate these challenging waters.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://www.binance.info/en-IN/register?ref=UM6SMJM3

I’m really glad to hear that my article helped you feel hopeful!