Which Risks are Not Covered Under the Fire Insurance Policy? Learn about the risks not covered under fire insurance policies and ensure you’re fully protected.

Introduction: Which Risks are Not Covered Under the Fire Insurance Policy?

Fire insurance policies are essential for businesses and homeowners, providing financial protection against fire-related losses. However, many policyholders are unaware that fire insurance policies don’t cover every risk. Understanding which Risks are Not Covered Under the Fire Insurance Policy? can help you avoid surprises and ensure you’re fully protected. In this blog post, we’ll explore the risks not covered under fire insurance policies and provide tips for getting the coverage you need.

What Risks are Not Covered Under Fire Insurance Policies?

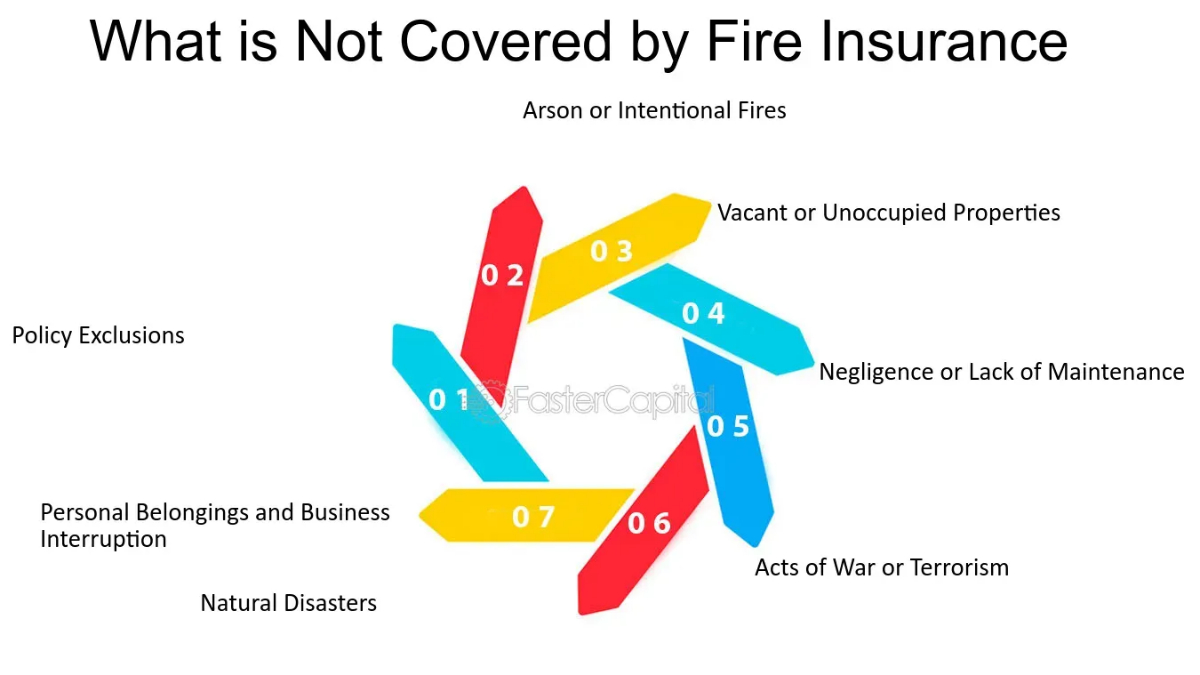

Which Risks are Not Covered Under the Fire Insurance Policy? Fire insurance policies do not cover certain risks, which include:

- Spontaneous combustion: Fire insurance policies typically exclude coverage for spontaneous combustion, which is a fire that ignites without an external heat source or ignition. This exclusion applies to incidents where heat-generating materials or substances, like oily rags, chemicals, or certain agricultural products, catch fire without an external ignition source.

- Acts of government or public authority: Damage caused by actions taken by government authorities, such as demolishing or burning a building for public safety reasons or permanent or temporary dispossession by order of the government, is not covered under fire insurance policies.

- Property undergoing any heating or drying process: This exclusion is included to limit the insurer’s liability in situations where the risk of fire is higher due to heating or drying processes. This could encompass activities like drying grains, textiles, or other materials, as well as heating processes used in various industries.

- The explosion of boilers (other than domestic boilers): The policy may provide a definition of what constitutes a boiler. This definition typically includes industrial and commercial boilers used in manufacturing, power generation, or other non-domestic applications. Domestic boilers, such as those used for heating homes, are usually not subject to this exclusion.

- Total or partial cessation of work: Fire insurance policies often exclude coverage for the total or partial cessation of work, also known as business interruption or loss of profits due to a fire-related incident.

- Normal cracking, settlement or bedding down of new structures: This exclusion generally applies to new structures or recently constructed buildings. It says the policy does not cover damage related to common, non-fire-related issues such as normal cracking, settlement, or bedding down of new structures.

- War or warlike operations, Nuclear perils: Damage caused by war, acts of terrorism, or nuclear events is often excluded from standard fire insurance policies.

- Pollution or contamination: The exclusion generally applies to losses or damages arising from pollution, contamination, or environmental hazards, regardless of whether they result from a fire or another cause.

- Overrunning, excessive pressure, short-circuiting, etc: This policy excludes coverage for damages related to specific electrical and mechanical issues, such as overrunning, excessive pressure, and short-circuiting.

- Wear and tear, gradual damage, and maintenance issues: Fire insurance generally does not cover damage caused by normal wear and tear, gradual deterioration, or lack of maintenance.

- Negligence: If the fire damage occurs as a result of the policyholder’s negligence, it may not be covered under the policy.

It is important to note that some of these risks can be covered by purchasing add-on covers or specialized policies. It is recommended to review the policy carefully and consult with an insurance expert to ensure that the coverage meets the specific needs of the policyholder.

How to Ensure You’re Fully Protected?

Read Your Policy Carefully

To ensure you’re fully protected, read your fire insurance policy carefully. Understand what’s covered and what’s not covered, and ask your insurance provider if you have any questions.

Consider Additional Coverage

If you live in an area prone to natural disasters, consider purchasing additional coverage. You may also want to consider a separate policy for pest control or damage from wear and tear.

Maintain Your Property

To avoid damage from wear and tear, maintain your property regularly. Fix any issues promptly to prevent further damage.

Review Your Policy Regularly

Review your fire insurance policy regularly to ensure it still meets your needs. If you’ve made any changes to your property, such as adding a new room or building a deck, update your policy to ensure you’re fully covered.

What is fire insurance and what does it cover?

Fire insurance is a type of property insurance that covers losses or damages caused by fire. It can provide financial protection for a wide range of assets, including buildings, equipment, inventory, and personal property. Fire insurance policies can be customized to suit your specific needs, with various types of policies, such as valued policy, average policy, and specific policy.

The scope of fire insurance coverage is broad and includes not only fire damage but also damage caused by lightning, bush fires, implosion or explosion, and aircraft damage. Fire insurance policies can also cover damages caused by natural disasters, including floods and earthquakes, but this may require additional coverage.

It is important to ensure that the sum insured is adequate and accurately represents the value of your property and belongings. You should also be aware of the policy term, deductibles, and claim process. Additionally, choosing a reputable and financially secure insurance company can provide peace of mind.

However, it is important to note that fire insurance policies do not cover all risks. For example, damage caused by war, nuclear accidents, or deliberate acts of the insured party are typically not covered. Therefore, it is essential to read the policy carefully and understand what is and is not covered to avoid any surprises in the event of a loss.

In summary, fire insurance is an essential type of property insurance that can provide financial protection against losses or damages caused by fire. It is important to choose the right type of policy and understand the coverage and exclusions to ensure that you are adequately protected.

What factors affect the cost of fire insurance?

Fire insurance premiums can be affected by various factors, including the value and reconstruction cost of the property, location, construction materials, fire protection systems, age of the property, deductibles, and claim history.

The value and reconstruction cost of the property are significant factors that influence fire insurance premiums. The more valuable the property, the higher the potential loss for the insurer, leading to higher premiums.

Location plays a crucial role in determining fire insurance premium rates. Properties located in areas prone to natural disasters, such as wildfires or earthquakes, or densely populated urban areas with a higher risk of fires, may face higher premiums.

Construction materials and fire protection systems can also impact fire insurance premiums. Properties made of fire-resistant materials, such as brick or stone, may attract lower premiums, while those made of flammable materials, such as wood, may face higher premiums. The presence of fire protection systems, such as sprinklers, smoke detectors, and fire alarms, can help prevent and detect fires, reducing the risk of damage and lowering premiums.

The age of the property can also affect fire insurance premiums, with older homes often facing higher premiums due to outdated electrical systems and older construction materials that are more flammable.

Deductibles and claim history can also influence fire insurance premiums. Choosing a higher deductible can lead to lower premiums, but it means that the policyholder will need to cover more expenses personally in case of a claim. A history of frequent or severe claims may lead to higher premiums, as insurers view policyholders with a history of claims as higher risks.

In summary, fire insurance premiums can be affected by various factors, including the value and reconstruction cost of the property, location, construction materials, fire protection systems, age of the property, deductibles, and claim history. Understanding these factors can help policyholders make informed decisions about their fire insurance coverage and potentially save money on premiums.

How to determine the value of a property for fire insurance purposes?

To determine the value of a property for fire insurance purposes, the reinstatement value method is typically used. This method calculates the cost of reinstating or replacing the property or assets with new ones of the same kind and quality, regardless of age or condition.

The reinstatement value method is based on the principle of indemnity, which means that the policyholder should be restored to the same financial position as before the loss or damage, no more and no less. This method requires the policyholder to declare the sum insured of the property or assets based on the reinstatement value, not the market value, and to pay a higher premium rate than the market value method.

To calculate the reinstatement value, the policyholder must consider the cost of materials, labor, and other expenses necessary to rebuild or replace the property or assets, such as architectural and engineering fees, debris removal, and compliance with building codes and regulations.

It is important to note that the reinstatement value method differs from the market value method, which calculates the cost of buying the property or assets in the open market after deducting depreciation or wear and tear.

To ensure that the sum insured is accurate and reflects the current market conditions, policyholders should consult with valuation experts or use government assessment tools to determine their property’s accurate market value. Regularly updating the valuation and incorporating changes such as renovations or market fluctuations into the insured value can help avoid underinsurance and mitigate the impact of the Average Clause.

In summary, to determine the value of a property for fire insurance purposes, the reinstatement value method is typically used, which calculates the cost of reinstating or replacing the property or assets with new ones of the same kind and quality, regardless of age or condition. Regularly updating the valuation and consulting with valuation experts or using government assessment tools can help ensure accuracy and avoid underinsurance.

What is the dynamo clause in fire insurance policies?

The Dynamo Clause in fire insurance policies refers to a provision that covers damage caused by electrical currents. This clause is a common inclusion in fire insurance policies and specifically addresses damages resulting from electrical issues like over-running, excessive pressure, short-circuiting, arcing, self-heating, or leakage of electricity, including lightning-related damage.

The Dynamo Clause is designed to provide coverage for losses or damages to electrical machines, apparatus, fixtures, or fittings due to electrical malfunctions or accidents. It is important for policyholders to understand the specifics of the Dynamo Clause in their fire insurance policy to ensure they are aware of the coverage provided for electrical-related incidents.

What is the purpose of the dynamo clause in fire insurance policies?

The purpose of the Dynamo Clause in fire insurance policies is to extend coverage to include losses or damages caused by electrical equipment like switches, lamps, dynamos, motors, or other electrical devices. Previously, insurance policies did not cover the equipment that sparked the fire, only paying for damages to other equipment and premises resulting from the fire.

However, with the Dynamo Clause, insurers now cover the equipment that caused the fire at an additional premium, ensuring that losses related to the electrical equipment triggering the fire are included in the coverage. This clause aims to address the exclusion of covering the equipment responsible for starting the fire, providing a more comprehensive protection for policyholders against losses caused by electrical malfunctions or accidents.

What is the additional premium for the dynamo clause in fire insurance policies?

The Dynamo Clause in fire insurance policies refers to a provision that covers damage caused by electrical currents, such as over-running, excessive pressure, short circuit, arcing, self-heating, or leakage of electricity, including lightning-related damage. This clause is designed to provide coverage for losses or damages to electrical machines, apparatus, fixtures, or fittings due to electrical malfunctions or accidents. It is an additional cover that can be appended to the Standard Fire and Special Perils (SFSP) policy by means of endorsement and by paying additional premiums.

The additional premium for the Dynamo Clause in fire insurance policies varies depending on the insurer and the terms of the policy. It is important for policyholders to understand the specifics of the Dynamo Clause in their fire insurance policy to ensure they are aware of the coverage provided for electrical-related incidents and the additional premium required for this coverage.

The Dynamo Clause is intended to protect insurance companies from having to pay for claims that are caused by the inherent electrical equipment, which is prone to malfunctions and can easily lead to fires. By excluding coverage for loss or damage caused by electrical currents, insurance companies can reduce their risk of having to pay for these claims. However, there are exceptions to the Dynamo Clause, such as if the electrical equipment is specifically mentioned in the policy or if the damage is caused by an insured peril.

In summary, the Dynamo Clause in fire insurance policies provides coverage for losses or damages to electrical machines, apparatus, fixtures, or fittings due to electrical malfunctions or accidents. This clause is an additional cover that requires an additional premium. It is important for policyholders to understand the specifics of the Dynamo Clause in their fire insurance policy to ensure they are aware of the coverage provided for electrical-related incidents and the additional premium required for this coverage.

What is the duration of the dynamo clause in fire insurance policies?

The duration of the Dynamo Clause in fire insurance policies typically lasts for the term of the policy for which it is endorsed. The Dynamo Clause is an additional cover that can be appended to the Standard Fire and Special Perils (SFSP) policy by means of endorsement and by paying additional premiums.

As long as the policy remains in force and the Dynamo Clause endorsement is active, the coverage for damages to electrical appliances caused by electrical currents, as specified in the clause, will be in effect. It is important for policyholders to review their policy documents and understand the specific terms and duration of the Dynamo Clause to ensure they are aware of the coverage provided and the period for which it is valid.

Perils that may be covered by fire insurance as an add-on:

Fire insurance policies can cover various perils, including fire, lightning, explosion/implosion, aircraft damage, riots, strikes, and terrorist activity, natural calamities like storms, cyclones, hurricanes, and floods, subsidence and landslide, bursting or overflowing of water tanks, pipes and apparatus, and bush fire. However, there are certain perils that are not covered by fire insurance policies unless add-on covers are bought for the specific risk, such as terrorism, earthquake, burglary, housebreaking, theft, etc.

Add-on covers can be purchased to extend the coverage of fire insurance policies to include these specific perils. For example, a business owner can purchase an add-on cover for terrorism to ensure that their business is protected against losses resulting from terrorist activities. Similarly, an add-on cover for earthquake can be purchased to protect the business against losses resulting from earthquakes.

The cost of add-on covers may vary depending on the insurer and the terms of the policy. It is important for policyholders to understand the specific terms and conditions of the add-on covers to ensure that they are adequately protected against the specific perils that they are concerned about. Consulting with an insurance expert can help businesses tailor their policies effectively to meet their unique needs and ensure comprehensive protection

Conclusion: Which Risks are Not Covered Under the Fire Insurance Policy?

Fire insurance policies are an essential part of protecting your property, but they don’t cover every risk. Understanding the limitations of your fire insurance policy can help you avoid surprises and ensure you’re fully protected.

By reading your policy carefully, considering additional coverage, maintaining your property, and reviewing your policy regularly, you can ensure you’re fully protected against fire-related losses.

FAQs: Which Risks are Not Covered Under the Fire Insurance Policy?

Q: What is fire insurance?

A: Fire insurance is a type of property insurance that covers damage or loss to property caused by fire and allied perils. It is designed to protect individuals and businesses from financial losses resulting from fire-related disasters.

Q: What are the benefits of fire insurance?

A: Fire insurance offers several benefits, including financial protection against unforeseen losses, reconstruction and replacement of damaged property, peace of mind, business continuity, legal compliance, and risk mitigation.

Q: What perils are covered under a fire insurance policy?

A: Fire insurance policies typically cover damage or loss caused by fire, lightning, explosion, implosion, impact, riot, strike, malicious damage, and burglary.

Q: What is the importance of fire insurance?

A: Fire insurance is important because it provides financial protection against the potentially crippling expenses resulting from fire-related disasters. It also promotes the implementation of fire prevention measures, as insurers often provide discounts for properties equipped with fire safety systems.

Q: What is the Dynamo Clause in fire insurance policies?

A: The Dynamo Clause is an add-on cover in fire insurance policies that provides coverage for damage caused by electrical currents, such as over-running, excessive pressure, short circuit, arcing, self-heating, or leakage of electricity, including lightning-related damage.

Q: What are the advantages of add-on covers in fire insurance policies?

A: Add-on covers in fire insurance policies provide additional benefits and protection to policyholders, such as coverage for consequential losses, additional expenses incurred during reconstruction, and coverage for specific perils like earthquake or flood.

Q: How can one choose the best fire insurance policy?

A: To choose the best fire insurance policy, individuals and businesses should assess their risk exposure and the value of the property to be insured, compare the features, benefits, and premiums of different fire insurance policies, check the claim settlement ratio and reputation of the insurance provider, and thoroughly review the policy document to understand the terms and conditions.

Q: What is the principle of proximate cause in fire insurance?

A: A replacement policy in fire insurance is a type of policy that covers the cost of replacing or repairing damaged or destroyed property with new items of the same kind and quality, rather than paying the actual cash value of the property. This type of policy ensures that the policyholder can replace their damaged property with new items, without having to worry about depreciation or wear and tear.

Q: What is covered in a Standard Fire and Allied Perils Policy?

A: A Standard Fire and Allied Perils Policy, also known as SFSP, covers the following perils: fire, lightning, explosion, implosion, impact damage due to insured’s own vehicle and articles dropped from them, riot, strike, malicious damage, and burglary. This policy provides coverage for damage caused by these perils to the insured property.

Q: Who Needs STFI Coverage in Fire Insurance?

A: STFI coverage, or Standard Fire and Allied Perils coverage, is recommended for anyone who owns property that is at risk of damage or loss due to fire or other allied perils. This type of coverage is particularly important for businesses, as it can help protect their assets and ensure that they can continue to operate in the event of a loss.

Q: What isn’t covered in fire insurance?

A: Fire insurance typically does not cover losses or damages caused by spontaneous combustion, burning of property by order of any public authority, property undergoing any heating or drying process, the explosion of boilers (other than domestic boilers), total or partial cessation of work, permanent or temporary dispossession by order of the government, normal cracking or settlement or bedding down of new structures, war or warlike operations, nuclear perils, pollution or contamination, overrunning, excessive pressure, short-circuiting, etc.

Q: What is not covered under standard fire and special perils policy?

A: The following perils are not covered under a standard fire and special perils policy:

Spontaneous combustion

Burning of property by order of any Public Authority

Property undergoing any heating or drying process

The explosion of boilers (other than domestic boilers)

Total or partial cessation of work

Permanent or temporary dispossession by order of the Government

Normal cracking or settlement or bedding down of new structures

War or warlike operations, Nuclear perils

Pollution or contamination

Overrunning, excessive pressure, short-circuiting, etc.

Q: Which of the following is not covered for homeowners?

A: The following perils are typically not covered for homeowners under a standard fire insurance policy:

Spontaneous combustion

Burning of property by order of any Public Authority

Property undergoing any heating or drying process

The explosion of boilers (other than domestic boilers)

Total or partial cessation of work

Permanent or temporary dispossession by order of the Government

Normal cracking or settlement or bedding down of new structures

War or warlike operations, Nuclear perils

Pollution or contamination

Overrunning, excessive pressure, short-circuiting, etc.

Q: What type of fires does insurance cover?

A: Insurance typically covers damage caused by fire, lightning, explosion, implosion, riot, strike, malicious damage, and burglary. However, it’s important to note that not all types of fires are covered. For example, fires caused by spontaneous combustion, burning of property by order of any public authority, property undergoing any heating or drying process, and the explosion of boilers (other than domestic boilers) are typically not covered.

Q: What is covered under all perils?

A: Under an all perils policy, damage caused by any peril not specifically excluded is covered. This type of policy provides comprehensive coverage for a wide range of risks, including fire, lightning, windstorm, hail, explosion, riot, civil commotion, vandalism, malicious mischief, and more. However, it’s important to note that not all perils are covered, and some may require additional coverage through endorsements or riders.

insurance | Auto Insurance Basics: With so many auto insurance options available, it’s important to choose coverage that fits your needs and driving habits. At MAFA Insurance, we emphasize the importance of comprehensive and collision coverage, especially for newer vehicles.

I’m really glad to hear that my article helped you feel hopeful!