Protect your business from lawsuits and accidents. Learn what commercial liability insurance covers and why you need it.

Introduction: Commercial Liability Insurance

Running a business is awesome. It’s your hard work, your dream taking shape. But, whoops – accidents happen. A customer slips on a wet floor, your product has an unexpected side effect, or someone takes a swipe at your reputation online. Without protection, these mishaps could cost you thousands, or even sink your business. That’s why we’re tackling commercial liability insurance with a no-nonsense, human-first approach. Let’s make sure your life’s work is protected!

What in the World is Commercial Liability Insurance?

Think of it like a safety net for your business against those “oops” moments. Here’s the gist:

- Bodily Injury: If a customer (or anyone, really) gets hurt on your premises or because of your work, it’ll help cover medical bills and legal costs if you get sued.

- Property Damage: Say a team member accidentally cracks a client’s fancy 80-inch TV while installing something. Liability insurance can help foot the repair or replacement bill.

- Advertising & Personal Injury: This one’s trickier. It covers things like slander, libel (written untruths), copyright mishaps in your advertising, etc. Basically, if someone’s reputation gets hurt because of your business actions, this helps.

Do I Really Need Commercial Liability Insurance?

Short answer: Most likely, YES! Here’s why:

- Lawsuits are Unpredictable: Even if you’re super careful, accidents happen, and people sue for all kinds of reasons (sometimes even frivolous ones!).

- Contracts Might Demand It: Many clients or landlords will require you to have liability insurance to work with them.

- Peace of Mind: Knowing you’ve got a financial cushion if things go haywire lets you focus on growing your business, not worrying.

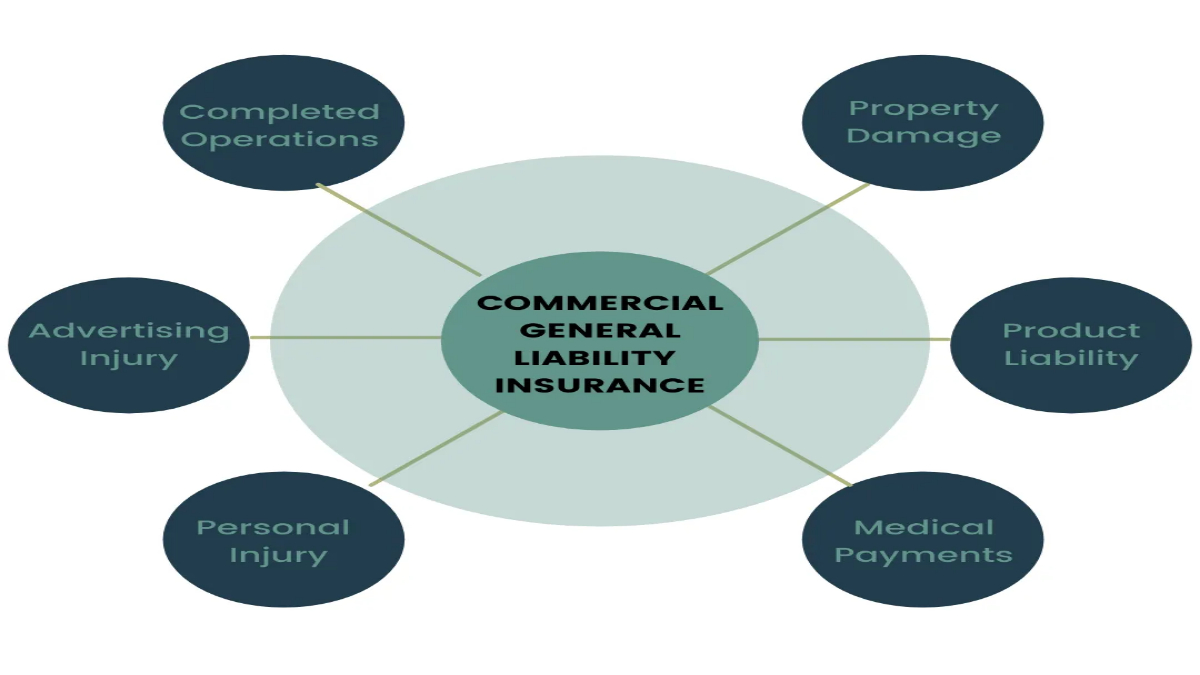

What Does Commercial Liability Insurance Typically Cover?

Let’s break down the common parts of a policy:

- Bodily Injury Liability

- H3: Medical Expenses (those doctor bills add up!)

- H3: Legal Defense Costs (Lawyers aren’t cheap)

- Property Damage Liability

- H3: Example: Your construction crew damages a fence on a neighboring property – insurance can come to the rescue!

- Products-Completed Operations Liability

- H3: Example: A product you manufactured months ago malfunctions and causes an injury.

- Personal and Advertising Injury

- H3: Examples include libel, slander, copyright infringement, and even wrongful eviction (if your business is a landlord).

Important Note: Every policy is different! This is a general overview.

What Doesn’t Commercial Liability Insurance Cover?

It’s not a magic shield against everything. Common exclusions include:

- Employee Injuries: That’s where workers’ compensation insurance comes in.

- Professional Mistakes: Look into errors & omissions insurance for that!

- Your Own Property/Equipment: You’ll need separate commercial property insurance.

- Intentional Acts: Don’t try to get insurance to pay for your wild weekend in Vegas. It won’t.

How Much Does Commercial Liability Insurance Cost?

Unfortunately, no one-size-fits-all answer here. Prices depend on factors like:

- Your Industry: High-risk jobs (construction) pay more than low-risk ones (office work).

- Business Size: Bigger businesses = more exposure = higher premiums.

- Location: Some states are more lawsuit-happy than others.

- Coverage Limits: How much protection do you want?

- Claims History: Lots of past claims make insurers nervous.

Types of Commercial Liability Insurance Policies

Confused yet? Don’t stress! Here’s the deal:

There are several different types of commercial liability insurance policies available, each designed to protect your business from specific types of risks. Here are some of the most common types of policies:

- General Liability Insurance: This is the most basic type of commercial liability insurance policy. It covers your business for bodily injury, property damage, and personal injury claims.

- Professional Liability Insurance: Also known as errors and omissions insurance, this policy covers your business for claims of professional negligence or failure to perform professional duties.

- Product Liability Insurance: This policy covers your business for claims of injury or damage caused by a product you sell or manufacture.

- Cyber Liability Insurance: This policy covers your business for claims of data breaches or cyber attacks.

- Employment Practices Liability Insurance: This policy covers your business for claims of discrimination, harassment, or wrongful termination.

Benefits of Commercial Liability Insurance Policies:

There are many benefits to having a commercial liability insurance policy for your business. Here are just a few:

Commercial liability insurance policies offer a wide range of benefits to businesses of all sizes. These policies can provide financial protection for your business in the event of property damage, bodily injury, or personal and advertising injury caused by your business operations or employees. Here are some of the key benefits of commercial liability insurance policies:

- Financial Protection: Commercial liability insurance policies can help protect your business from financial loss resulting from property damage, bodily injury, or personal and advertising injury caused by your business. This can provide peace of mind and help ensure that your business is able to continue operating even in the face of unexpected events.

- Legitimacy and Trust: Carrying commercial liability insurance can signify a level of legitimacy for your business that can lessen concerns from potential business associates and clients. It can also help build trust and encourage clients to work with you, as they know that you have insurance coverage in place to protect them.

- Reputation and Growth: Commercial liability insurance can positively impact business reputation and growth by demonstrating that you are willing to assume responsibility for accidents that occur on the job and that you have your customers’ best interests in mind. This can lead to increased trust, recommendations, and repeat business.

- Legal Protection: Commercial liability insurance can provide protection for legal expenses in the event that your business has a liability claim brought against it. This can help ensure that you are able to defend your business and protect your assets in the event of a lawsuit.

- Customizable Coverage: Commercial liability insurance policies can be customized to fit the specific needs of your business. This can help ensure that you have the coverage you need to protect your business from a wide range of risks.

In summary, commercial liability insurance policies offer a wide range of benefits to businesses of all sizes. These policies can provide financial protection, build trust and legitimacy, positively impact reputation and growth, provide legal protection, and be customized to fit the specific needs of your business. If you are a business owner, it is important to consider the benefits of commercial liability insurance and to work with an insurance professional to determine the right coverage for your business.

Which One is Right for Me?

That depends on your business. Occurrence-based is generally safer for long-lasting risks (like with manufactured products). Claims-made is common for temporary or project-based work. An insurance agent can help you decide.

How to Choose the Right Commercial Liability Insurance Policy?

Choosing the right commercial liability insurance policy for your business can be a complex process. Here are some things to consider:

- Type of business: The type of business you have will determine the type of policy you need. For example, if you sell products, you’ll need product liability insurance.

- Size of business: The size of your business will also impact the type of policy you need. Larger businesses may need more comprehensive coverage than smaller businesses.

- Risk factors: Consider the risks associated with your business. For example, if you have a lot of foot traffic in your store, you may need more coverage for bodily injury claims.

- Budget: Consider your budget when choosing a policy. While it’s important to have coverage, you don’t want to pay for more than you need.

What are the consequences of not having commercial liability insurance?

Not having commercial liability insurance can have serious consequences for businesses. The consequences of not having business insurance include the immediate loss of income for your business in the event of a claim, unrecoverable loss of equipment, large legal fees, and legal trouble. If your business comes into close contact with the public on a regular basis or has employees, there’s always a risk that someone will be injured either at work or as a result of the work going on. Without insurance, you’ll be facing potentially large legal fees if someone makes a claim against your company for negligence.

In the UK, some types of business insurance are mandatory, and not having them can land you in serious legal trouble. For example, if you have employees, you must have employers’ liability insurance by law. This covers you and your business in the event an employee is injured or becomes ill as a result of working for your company. If you don’t have employers’ liability insurance when you should, you run the risk of facing large fines.

Not having commercial liability insurance can also put your business’s future at risk. While having business insurance can often feel like an expense, like house or car insurance, if something goes wrong, you’ll be in a better position with insurance in place. Finding the right level of business insurance can protect your company against any and all unforeseen circumstances and cover the costs of repairing or replacing damaged equipment, lost income, and legal fees. Without business insurance, your business is always at risk of failing because you won’t be able to survive if the worst does happen.

In summary, not having commercial liability insurance can lead to significant financial losses, legal trouble, and even the failure of your business. It’s essential to have the right level of business insurance to protect your company against any and all unforeseen circumstances and ensure its future success.

How can a lack of commercial liability insurance affect a business’s reputation?

A lack of commercial liability insurance can have significant consequences for a business’s reputation. When a business does not have liability insurance, it may be seen as a riskier partner to work with, as there is no financial protection in place in case of accidents or damages. This can make it more difficult for the business to attract and retain clients or customers, as they may be hesitant to work with a company that does not have insurance coverage.

Additionally, if a business without liability insurance is involved in a legal dispute or lawsuit, it may be required to pay for any damages or legal fees out of pocket. This can be a significant financial burden for the business, and it may struggle to recover from the costs. This can also lead to negative publicity for the business, which can further damage its reputation.

On the other hand, having commercial liability insurance can help protect a business’s reputation by providing financial protection in case of accidents or damages. This can give clients and customers peace of mind knowing that the business is financially responsible and able to cover any costs associated with accidents or damages. It can also help the business avoid negative publicity and legal disputes, which can help protect its reputation.

In summary, a lack of commercial liability insurance can have significant consequences for a business’s reputation, including difficulty attracting and retaining clients or customers, financial burden in case of legal disputes or lawsuits, and negative publicity. Having commercial liability insurance can help protect a business’s reputation by providing financial protection and avoiding negative consequences.

Who Sells Commercial Liability Insurance?

- Independent Agents: These folks work with multiple companies, helping you compare.

- Direct Insurers: You deal straight with the company (think GEICO, Progressive, etc.)

- Specialty Insurers: They focus on specific industries (construction, tech, etc.), offering tailored policies.

Tips for Choosing a Commercial Liability Insurance Policy

- The Right Coverage: Assess your business risks carefully; don’t skimp where you need protection.

- Financial Strength of the Insurer: Check ratings (like A.M. Best). You want a company that will actually pay up if disaster strikes.

- Reputation and Customer Service: Read online reviews. In a crisis, you need an insurer that has your back.

- Don’t Just Look at Price: Balance cost with coverage and the company’s reliability.

Specific Industry Examples

- Construction: High-risk work means these businesses need robust liability coverage – everything from injuries on site to faulty workmanship claims.

- Tech Companies: Their focus is more on things like data breaches, intellectual property disputes, and professional errors

- Restaurants: Slip and falls, food contamination, liquor liability… there’s a lot that can go wrong!

- Retail Stores: Customer injuries, product liability, advertising mishaps – it’s a broad field of risk.

We could pick one industry and dissect specific real-world scenarios and what kind of coverage would apply.

Advanced Coverage Options

- Umbrella Liability Coverage: Got a big business or extra high risks? Umbrella insurance adds a giant layer of protection above and beyond your standard liability limits.

- Employment Practices Liability Insurance (EPLI): Protection against lawsuits from employees alleging discrimination, harassment, wrongful termination, etc.

- Directors & Officers Liability (D&O): If you run a larger company, this protects board members from personal liability if they’re sued over company decisions.

The Claims Process

- What happens when a claim gets filed? This is where policyholders often feel overwhelmed. We could break down the steps, explain common terms, and offer tips for navigating the process.

Finding Expert Help

- How to work effectively with an insurance agent or broker. What questions to ask, what red flags to watch for, etc.

Conclusion:

Commercial fire insurance coverage is an essential investment for any business owner looking to protect their assets and investments from potential fire hazards. By understanding the basics of commercial fire insurance coverage, you can make informed decisions about the right policy for your business. At [Insurance Company], we’re here to help you find the right commercial fire insurance coverage for your business. Contact us today to learn more.

My brother recommended this blog to me, and he was absolutely correct. This post truly brightened my day. You wouldn’t believe the amount of time I had dedicated to finding this information. Thank you!