Explore the intricacies of Health Insurance Claim Settlement Ratios in 2024, learn about the highest CSR, ideal ratios, calculation methods, and more in this detailed guide.

Introduction: Health Insurance Claim Settlement Ratios (CSR) in 2024

Navigating the Health Insurance Claim Settlement Ratios can be complex, especially when it comes to understanding how effectively insurance companies handle claims. The Claim Settlement Ratio (CSR) is a crucial metric that helps policyholders gauge the reliability of insurance companies. This blog post delves into the nuances of CSR, highlighting the highest ratios in 2024, explaining ideal ratios, and providing a step-by-step guide on how to calculate these figures. Whether you’re a policyholder or considering purchasing health insurance, this guide will equip you with the knowledge to make informed decisions.

What is Health Insurance Claim Settlement Ratio (CSR)?

Definition and Importance

The Claim Settlement Ratio is a measure used to evaluate the efficiency and reliability of an insurance company in handling claims. It is defined as the percentage of insurance claims an insurer has paid out during a financial year compared to the total claims received. For policyholders, a higher CSR indicates a greater likelihood of their claims being settled, which can be a critical factor in choosing an insurer.

How CSR Impacts Policyholders

A high CSR not only reflects an insurer’s financial health but also its commitment to serving its policyholders. It reassures customers that their claims are likely to be handled efficiently and fairly, providing peace of mind and enhancing trust in the insurer.

Which Insurance Has the Highest Claim Settlement Ratio in 2024?

In 2024, Care Health Insurance stands out with a remarkable CSR of 100%, indicating its exceptional reliability in settling claims promptly and effectively.

What is the Ideal Claim Settlement Ratio?

Understanding the Ideal CSR

The ideal Claim Settlement Ratio is typically 90% or above. This range assures policyholders that the majority of claims are settled, reflecting the insurer’s good faith and reliability.

How Do You Calculate Insurance Claim Ratio?

Step-by-Step Calculation

To calculate the Claim Settlement Ratio, divide the number of claims settled by the insurer by the total number of claims received within the same period, then multiply by 100 to express it as a percentage.

Example:

If an insurer receives 1,000 claims and settles 950, the CSR would be:

CSR=(9501000)×100=95%CSR=(1000950)×100=95%

What is a Good Claims Ratio?

A good claims ratio, or loss ratio, typically falls between 60% and 80%. This range indicates that the insurer is effectively using premiums to settle claims while maintaining financial stability.

What Insurance Company Denies the Most Claims?

While specific data on claim denials by company is proprietary, industry reports and consumer feedback suggest that variability exists across insurers. Policyholders are encouraged to research insurers’ reputations for claim handling before purchasing policies.

What is a Good Claims Closing Ratio?

A good claims closing ratio is close to 1.0, indicating that the insurer is closing nearly as many claims as it opens, which signifies efficient claims management.

What is the 100 Claim Settlement Ratio?

A 100% Claim Settlement Ratio means that the insurer has settled every claim received within a financial year, showcasing exceptional customer service and reliability.

What is the Difference Between Claim Ratio and Claim Settlement Ratio?

While both metrics relate to claims, the claim ratio (or loss ratio) measures the percentage of premiums used to settle claims, whereas the CSR measures the percentage of claims settled out of the total received.

How to Calculate Insurance Claim Settlement?

The calculation method for insurance claim settlement involves determining the amount the insurer needs to pay based on the policy terms. This calculation considers deductibles, co-payments, and coverage limits.

What is the difference between loss ratio and combined ratio?

The difference between the loss ratio and the combined ratio in the insurance industry primarily lies in the components each ratio includes to assess the profitability and financial health of an insurance company.

Loss Ratio:

The loss ratio measures the total incurred losses in relation to the total collected insurance premiums. It is calculated by dividing the total incurred losses by the total collected insurance premiums. This ratio focuses solely on the losses paid out in claims and does not account for any other operational expenses of the insurance company.

Combined Ratio:

The combined ratio, on the other hand, measures both the incurred losses and the operational expenses in relation to the total collected premiums. It is essentially calculated by adding the loss ratio and the expense ratio. The expense ratio includes all other expenses related to the operation of the insurance business, such as administrative and marketing expenses. A combined ratio below 100 percent indicates that the company is making an underwriting profit, while a ratio above 100 percent suggests that the company is paying out more in claims and expenses than it is receiving from premiums.

In summary, while the loss ratio provides insight into the losses an insurer incurs from claims relative to the premiums it collects, the combined ratio offers a more comprehensive view by also including the insurer’s operational expenses. This makes the combined ratio a more inclusive measure of an insurance company’s overall profitability and financial health.

How is the loss ratio calculated?

The loss ratio is calculated by adding the total incurred losses (which include both claims paid and reserved) and the loss adjustment expenses, then dividing this sum by the total premiums earned during the same period. This calculation is expressed as a percentage.

For example, if an insurance company pays $60,000 in claims, reserves an additional amount for future claims, spends $5,000 on adjusting claims, and earns $100,000 in premiums, the loss ratio would be calculated as follows:

Loss Ratio=($60,000+$5,000$100,000)×100=65%Loss Ratio=($100,000$60,000+$5,000)×100=65%

This formula shows that the insurance company used 65% of its premiums to cover claims and expenses related to those claims.

What is the formula for calculating the combined ratio?

The formula for calculating the combined ratio is given by adding the underwriting loss ratio and the expense ratio. This can be represented as:

Combined Ratio=Underwriting Loss Ratio+Expense Ratio

Where:

- The Underwriting Loss Ratio is calculated as (Claims paid+Net loss reserves)/Net premium earned(Claims paid+Net loss reserves)/Net premium earned

- The Expense Ratio is calculated as Underwriting expenses/Net premium writtenUnderwriting expenses/Net premium written

Underwriting expenses include costs such as agents’ commissions, staff salaries, marketing expenses, and other overhead expenses.

How do insurance companies use the combined ratio to evaluate profitability?

Insurance companies use the combined ratio as a key metric to evaluate their profitability and overall financial health. The combined ratio is calculated by adding the loss ratio and the expense ratio together. This ratio provides a comprehensive view of the costs associated with an insurance company’s operations in relation to the premiums it earns.

Calculation of the Combined Ratio:

The combined ratio is expressed as a percentage and is calculated by the formula:

Combined Ratio=Loss Ratio+Expense Ratio

where:

- Loss Ratio is calculated as the total incurred losses (including claims paid and adjustments) divided by the total earned premiums.

- Expense Ratio includes all operational expenses (such as administrative costs, salaries, and commissions) divided by the earned premiums.

Interpreting the Combined Ratio:

- A combined ratio below 100% indicates that the insurance company is making an underwriting profit, meaning that the premiums collected exceed the sum of incurred losses and operational expenses. This scenario suggests financial health and operational efficiency.

- A combined ratio above 100% indicates an underwriting loss, meaning that the costs (losses and expenses) exceed the premiums earned. This situation points to potential issues in pricing, claims management, or operational efficiency that could affect the company’s profitability.

Importance of the Combined Ratio:

- The combined ratio is crucial for assessing the profitability of insurance companies because it directly reflects the balance between income (from premiums) and expenditures (claims and operating costs).

- It helps stakeholders, including investors and regulators, understand how well an insurance company is managing its underwriting practices and expenses.

- Insurance companies strive to maintain a combined ratio as low as possible to ensure profitability and sustainability. Strategies to improve the combined ratio include enhancing underwriting standards, efficient claims management, and controlling operational costs.

In summary, the combined ratio is a fundamental indicator used by insurance companies to evaluate their profitability and operational efficiency. A ratio below 100% is generally favorable and indicates profitability, while a ratio above 100% may signal financial distress or inefficiencies in the company’s operations.

How can i calculate the loss ratio for an insurance company?

To calculate the loss ratio for an insurance company, you can use the following formula:

Here’s a step-by-step breakdown of how to use this formula:

- Determine the Insurance Claims Paid: This is the total amount of money the insurance company has paid out to policyholders for claims during a specific period.

- Determine the Loss Adjustment Expenses: These are the expenses incurred by the insurance company to assess and process claims. This includes costs related to investigating, validating, and settling claims.

- Determine the Total Premiums Earned: This is the total amount of premiums that the insurance company has collected from policyholders during the same period.

- Calculate the Loss Ratio: Add the Insurance Claims Paid and the Loss Adjustment Expenses together. Divide this sum by the Total Premiums Earned. Multiply the result by 100 to convert it into a percentage.

Example Calculation:

Suppose an insurance company has the following figures for a given year:

- Insurance Claims Paid: $60,000,000

- Loss Adjustment Expenses: $5,000,000

- Total Premiums Earned: $100,000,000

Using the formula:

Loss Ratio=($60,000,000+$5,000,000$100,000,000)×100=65%Loss Ratio=($100,000,000$60,000,000+$5,000,000)×100=65%

This calculation shows that the insurance company used 65% of its premiums to cover claims and related expenses.

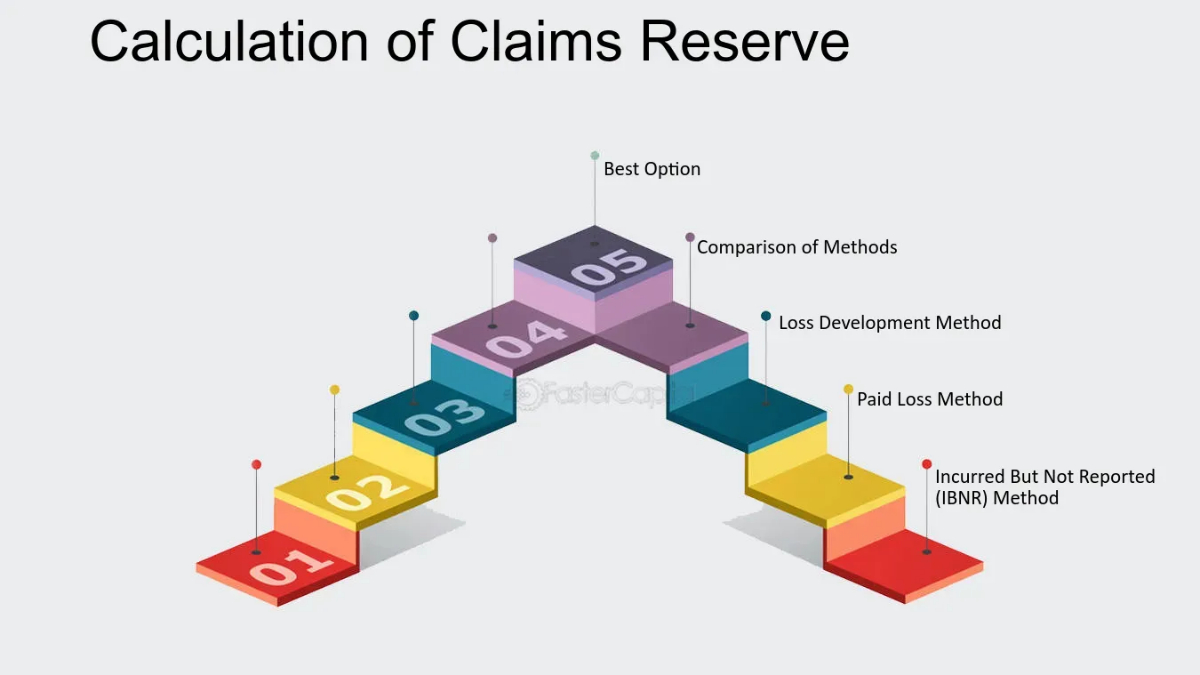

What is the claims reserve and how is it calculated?

A claims reserve is an amount of money set aside by an insurance company to pay for future claims that have been incurred but not yet settled or reported. This reserve is crucial for ensuring that an insurance company has sufficient funds to cover its obligations towards policyholders who have filed or are expected to file legitimate claims. The process of funding a claims reserve is based on projections of the amount of money needed to settle both unsettled claims and claims that have occurred but have not yet been reported (IBNR).

The calculation of a claims reserve involves several steps and can be based on various methods, including actuarial estimates. These estimates take into account the company’s experience with claims over the years and the amount of losses the company has incurred in the past. Additionally, individual experience of the adjuster helps in adjusting the reserve according to the adjuster’s experience with the company’s claims.

One common method used for estimating claims reserves is the Chain Ladder Method (CLM), which projects past claims experience into the future to forecast the amount of reserves that must be established to cover projected future claims. This method operates under the assumption that patterns in claims activities in the past will continue to be seen in the future. The CLM calculates incurred but not reported (IBNR) loss estimates using run-off triangles of paid losses and incurred losses, representing the sum of paid losses and case reserves.

The steps involved in applying the Chain Ladder Method include13:

- Compile claims data in a development triangle.

- Calculate age-to-age factors.

- Calculate averages of the age-to-age factors.

- Select claim development factors.

- Select tail factor.

- Calculate cumulative claim development factors.

- Project ultimate claims.

Age-to-age factors, also known as loss development factors (LDFs) or link ratios, represent the ratio of loss amounts from one valuation date to another. These factors are intended to capture growth patterns of losses over time and are used to project where the ultimate amount of losses will settle.

In summary, a claims reserve is established by insurance companies to ensure they can meet future claim obligations. The calculation of this reserve is based on projections and actuarial estimates, with methods like the Chain Ladder Method being commonly used to forecast future claims based on past experience.

Conclusion: Health Insurance Claim Settlement Ratios

In conclusion, understanding the concept of Health Insurance Claim Settlement Ratios reserves is essential for the financial stability and operational integrity of insurance companies. Claims reserves represent the estimated funds that an insurer needs to set aside to cover future claim payouts, including those that have been reported but not yet settled, and those incurred but not reported (IBNR). Accurately calculating these reserves is crucial because it impacts the insurer’s ability to meet its financial obligations and maintain solvency.

Various methods, such as the Chain Ladder Method, are employed to estimate these reserves based on historical data and projected future claims. These calculations involve sophisticated actuarial techniques and statistical models to ensure that the reserves are sufficient to cover all future claims.

For insurance companies, maintaining accurate claims reserves not only complies with regulatory requirements but also builds trust with policyholders by ensuring that claims can be paid out promptly and fairly. For policyholders, understanding the role of claims reserves can provide insights into the financial health of their insurers and the reliability of coverage in times of need.

Overall, the management of claims reserves is a dynamic area that requires continuous monitoring and adjustment based on emerging data and trends in claim frequencies and severities. It is a critical aspect that underscores the importance of robust risk management practices within the insurance industry.